Articles

- BLOG / Articles / View

- Articles

Monday Macro View: Basin-by-Basin Trends

By Osama on March 23, 2026 in Market Sentiment

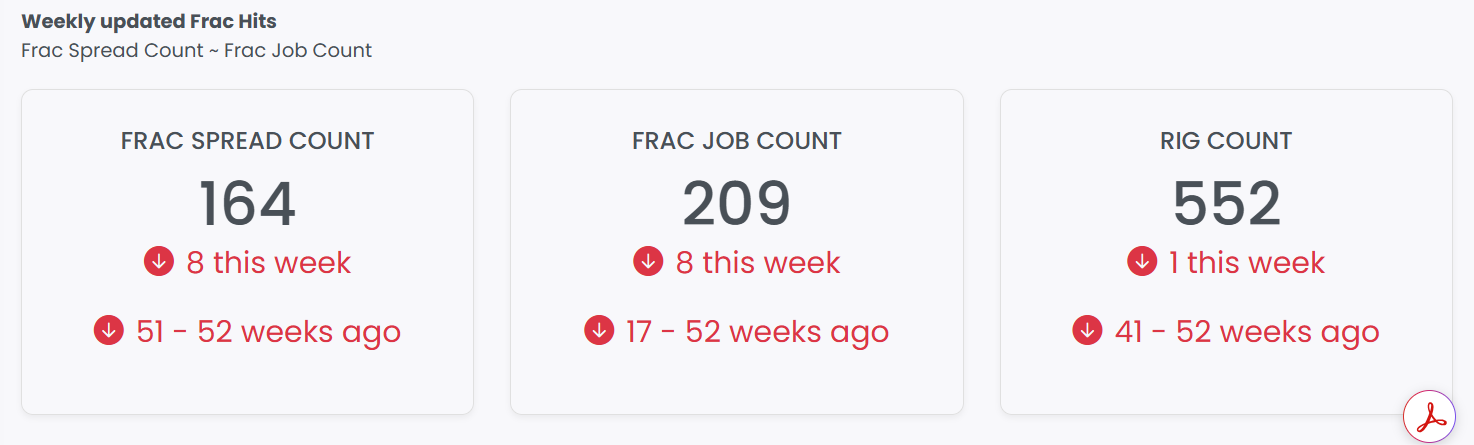

The Frac Spread Count (FSC) for the week ending March 20 came in at 164, reflecting a week-on-week decline of 8. The Frac Job Count (FJC) mirrored that movement, dropping by 8 as well to stand at 209. While the pullback may draw attention at first glance, it should be contextualized within the broader trend: activity had been registering consecutive upticks for more than three weeks prior to this reading, suggesting this week's softness is more of a routine consolidation than a directional reversal. Seasonal patterns and operational scheduling between operators can account for single-week fluctuations of this magnitude, and the overall activity level remains within the range observed over the past month.

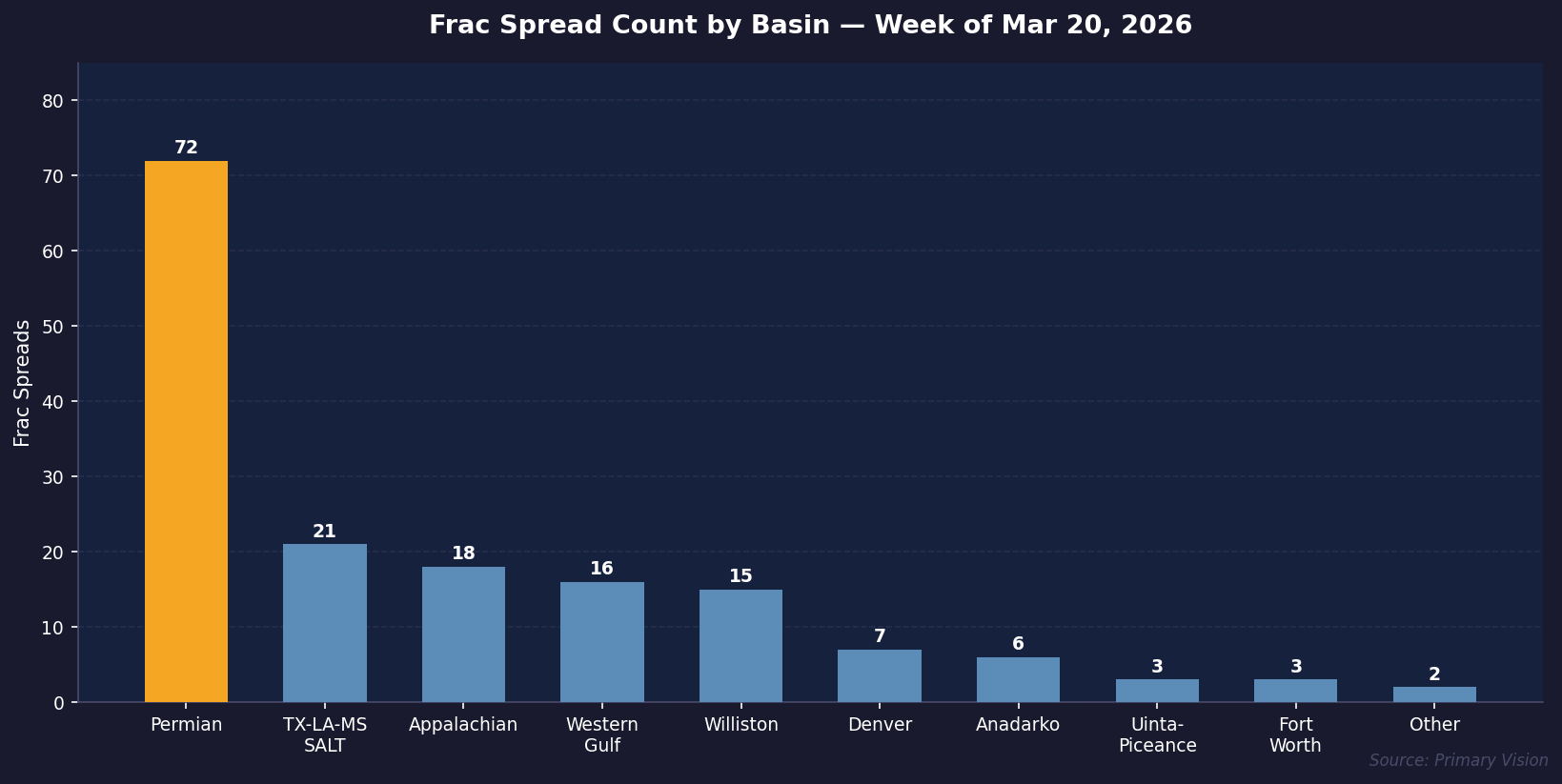

At the basin level, the most notable movement this week was in the Permian, which slipped to 72 spreads from 76 where it had held steady for the prior two weeks — a decline of 4 and the single largest basin-level change in the data this week. The TX-LA-MS SALT basin, which captures completions activity across the salt basin plays of East Texas, Louisiana, and Mississippi — including the Haynesville — ticked up to 21 from 20, a modest but directionally positive move for a region heavily weighted toward natural gas production. That uptick is notable given the current macro backdrop: benchmark natural gas prices have risen sharply since late February, driven by the geopolitical disruption stemming from strikes on Iran's South Pars gas field and the retaliatory damage sustained by Qatar's Ras Laffan LNG complex, which has taken an estimated 17% of Qatar's LNG export capacity offline. Henry Hub futures have responded accordingly. It is worth noting, however, that completions activity typically lags price signals by several weeks, meaning the full operator response to the current gas price environment is unlikely to be visible in FSC data yet. The Appalachian basin — the other major gas-focused play and the largest single source of U.S. natural gas production — held steady at 18 for the third consecutive week, suggesting operators there are maintaining a measured pace for now, even as longer-term demand drivers including LNG export growth and data center power load remain structurally supportive.

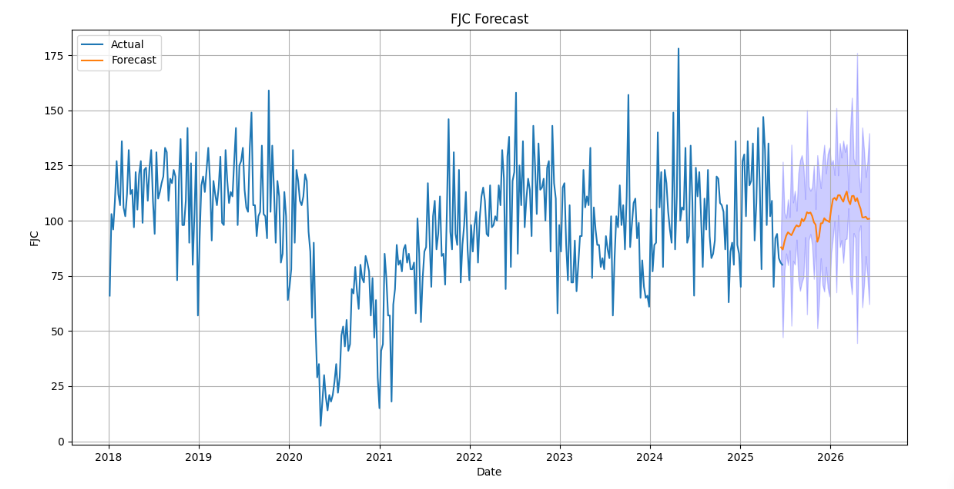

On the FJC side, the basin-level forecast data adds a dimension that the weekly actuals alone do not convey. The Permian, which printed 103 this week, is forecast to partially recover to 109 — but the yearly change of -33 is the more consequential number. This is not weekly noise; it points to a basin undergoing a structural reduction in completions intensity year-on-year, with downstream implications for associated gas volumes that remain to be fully priced into supply outlooks.

Source: Frac Job Count Forecast over next 52 week for Permian Basin - EFRACS by Primary Vision

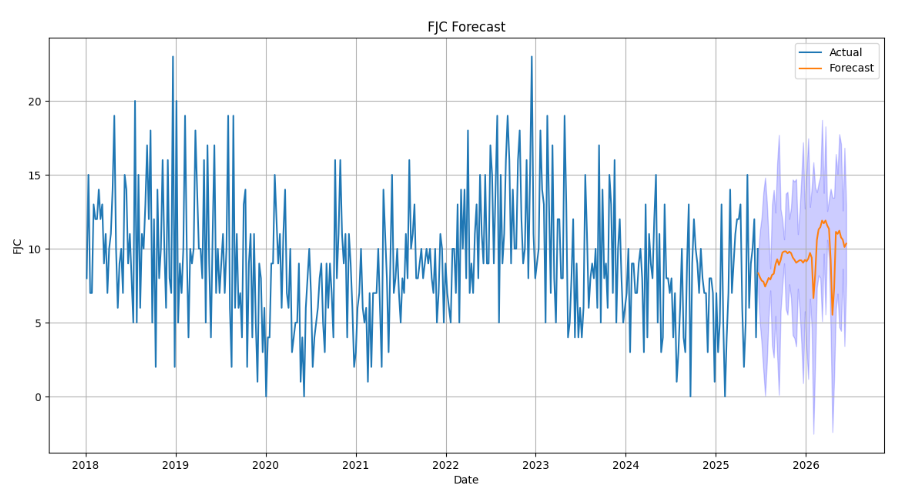

The Haynesville, by contrast, is forecast to climb from its current 9 to 12, with a yearly change of +3 — the only gas-focused basin in this dataset showing positive year-on-year momentum. Whether the current geopolitical-driven gas price environment accelerates that trajectory beyond what the model currently anticipates remains to be seen, but the directional setup is constructive. Appalachian is perhaps the most underappreciated signal here: forecast at 15 with a yearly change of -11, the basin is seeing completions activity compress even as it anchors U.S. gas supply. How long production holds at current levels against a falling completions base is a question that will matter significantly over the next four to six quarters.

Source: Frac Job Count Forecast over next 52 week for Haynesville Basin - EFRACS by Primary Vision

The United States enters the second quarter as the most consequential swing supplier in a global gas market restructured almost overnight. The domestic completions picture has not yet fully responded — but that is precisely the opportunity. Permian resilience, a Haynesville on an upward forecast trajectory, and an Appalachian basin still anchoring national supply despite a tightening completions base all point to an industry with meaningful room to accelerate. The global disruption has done what no domestic policy conversation could: it has created durable, urgent, and structural demand for U.S. gas. The completions market is coiled. Watch this space.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform