Market Sentiment Tracker: They Were Wrong About Rate Cuts. Again.

By

Osama

on March 24, 2026

in

Market Sentiment

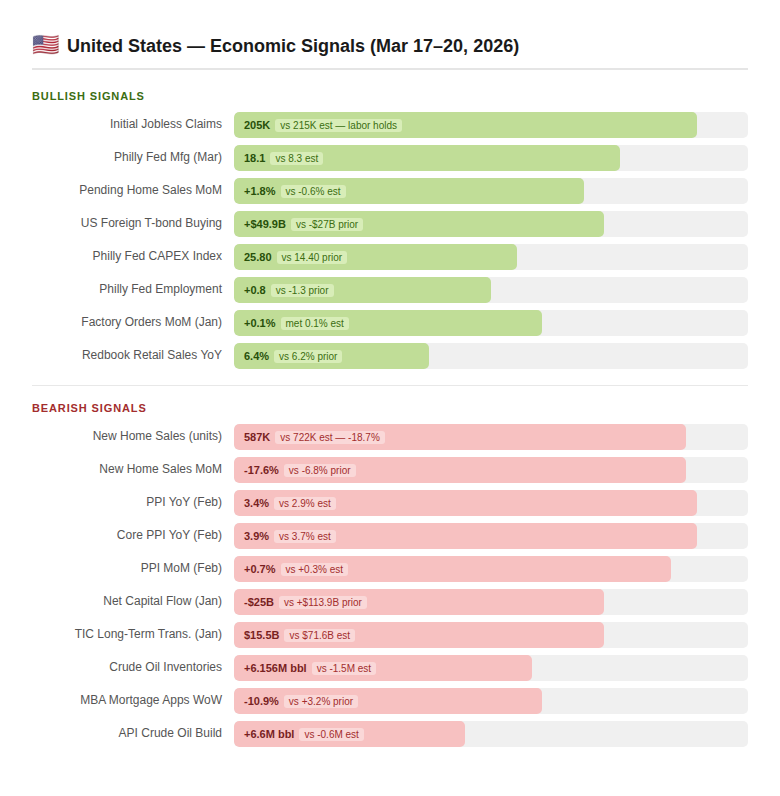

United States — Inflation Won't Let the Fed Breathe

The world repriced rate expectations this week. The 10-year Treasury hit 4.40% as markets abandoned hopes for multiple 2026 rate cuts, and the week's US data explained why. PPI came in at 0.7% MoM — more than double the 0.3% consensus — pushing the annual reading to 3.4%. Core PPI sits at 3.9%. These aren't rounding errors; they're a Fed that has no political cover to ease. The March dot plot showed seven of nineteen FOMC participants expecting rates to stay unchanged all year, and this week's numbers will only harden that camp.

Source: Primary Vision | Note: Each color in the bar represents the importance of the factor to the real economy

The tragedy is what higher-for-longer is doing to housing. New home sales collapsed to 587K against a 722K consensus — a near 19% miss — with mortgage applications down 10.9% in the same week. J.P. Morgan now projects home prices to stall at 0% in 2026, with affordability structurally broken for first-time buyers at 6.30% rates. Meanwhile the Philly Fed CAPEX index nearly doubling and jobless claims printing well below estimates confirm that AI-driven industrial investment is insulating one half of the economy completely. The US isn't slowing — it's splitting.

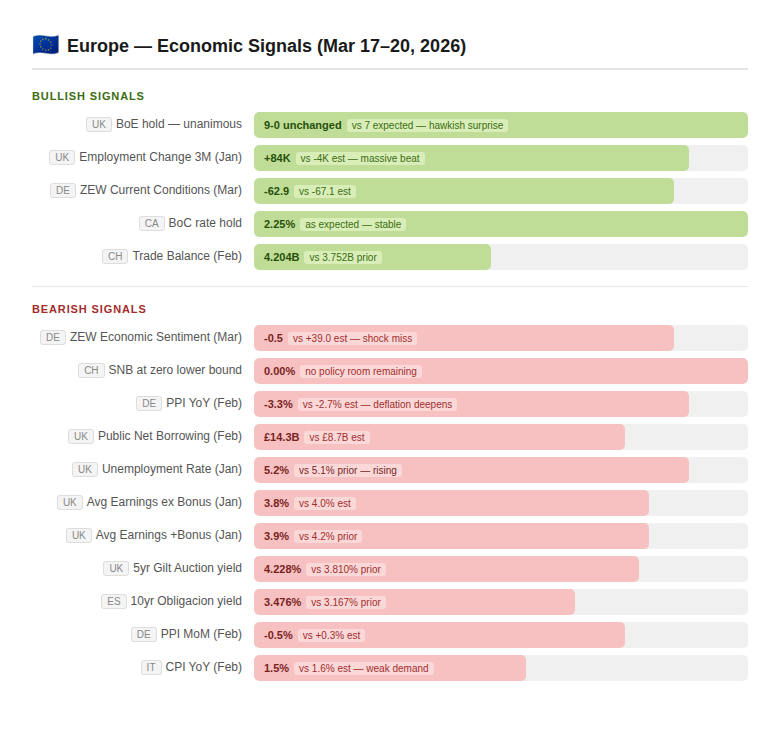

Europe — The Recovery Story Just Got Harder to Believe

Europe entered 2026 carrying genuine hope: Germany's €500 billion fiscal package, defence spending acceleration, and an ECB that had stopped tightening. Rabobank flagged that the fiscal investment agenda would push long-term eurozone yields higher as debt issuance rises — a cost Europe was willing to absorb in exchange for growth. The ZEW Economic Sentiment collapsing to -0.5 against a +39.0 consensus this week signals that institutional investors have stopped believing the recovery arrives on schedule.

Source: Primary Vision | Note: Each color in the bar represents the importance of the factor to the real economy

The deeper problem is that S&P Global's March outlook explicitly flags Germany, the UK, and Japan as economies where even a moderately persistent energy shock would likely tip growth into recession — and European gas prices are already moving. German PPI deepening to -3.3% YoY means the industrial core is deflating while sovereign funding costs are rising simultaneously: UK gilt yields jumped from 3.810% to 4.228% in a single week. The BoE holding unanimously at 3.75% — when two cuts were expected — confirms policymakers see inflation risk as unresolved. High government debt and elevated sovereign yields are now structurally limiting fiscal options across advanced Europe. The fiscal ambition is real. The execution window is narrowing fast.

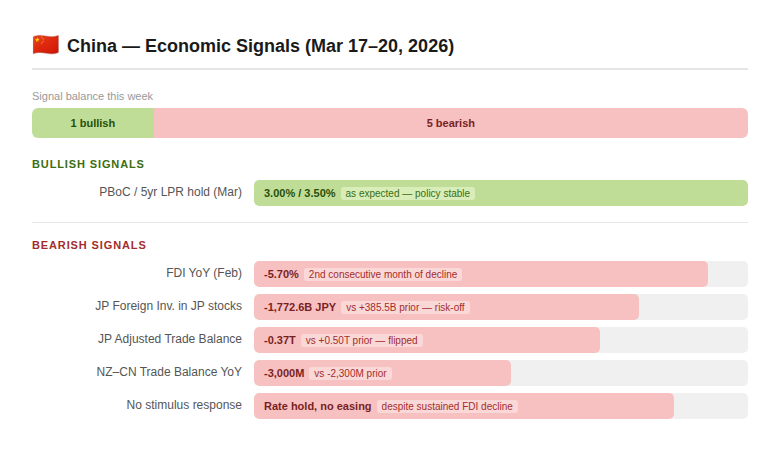

China — Capital Doesn't Wait for Policy Clarity

Most major advanced-economy central banks are nearing the end of their rate-cutting cycles, with mounting global debt keeping long-term rates structurally elevated — and this global backdrop is hitting China from an angle Beijing can't directly control. When US rates stay high, the return differential between dollar assets and Chinese assets widens, and capital flows accordingly. FDI contracting at -5.70% for a second consecutive month, with no stimulus response from the PBoC, is a symptom of exactly that dynamic.

Source: Primary Vision | Note: Each color in the bar represents the importance of the factor to the real economy

China's inward FDI fell to just $4.5 billion in 2024 — the lowest since 1991 — representing barely 1.3% of its 2021 peak, and the trajectory into 2026 has not reversed. The regional spillover is visible: Japan's foreign equity investment swung from +385.5B yen to -1,772.6B yen, and the adjusted trade balance flipped into deficit. These aren't isolated readings — they reflect a consistent withdrawal of engagement with the China-anchored regional economy. The IMF identifies policy uncertainty and geopolitical risk as the primary structural drivers of the FDI decline — neither of which a passive rate hold addresses. Beijing is holding its position while the conditions that drive capital away remain firmly in place.

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform