Articles

- BLOG / Articles / View

- Articles

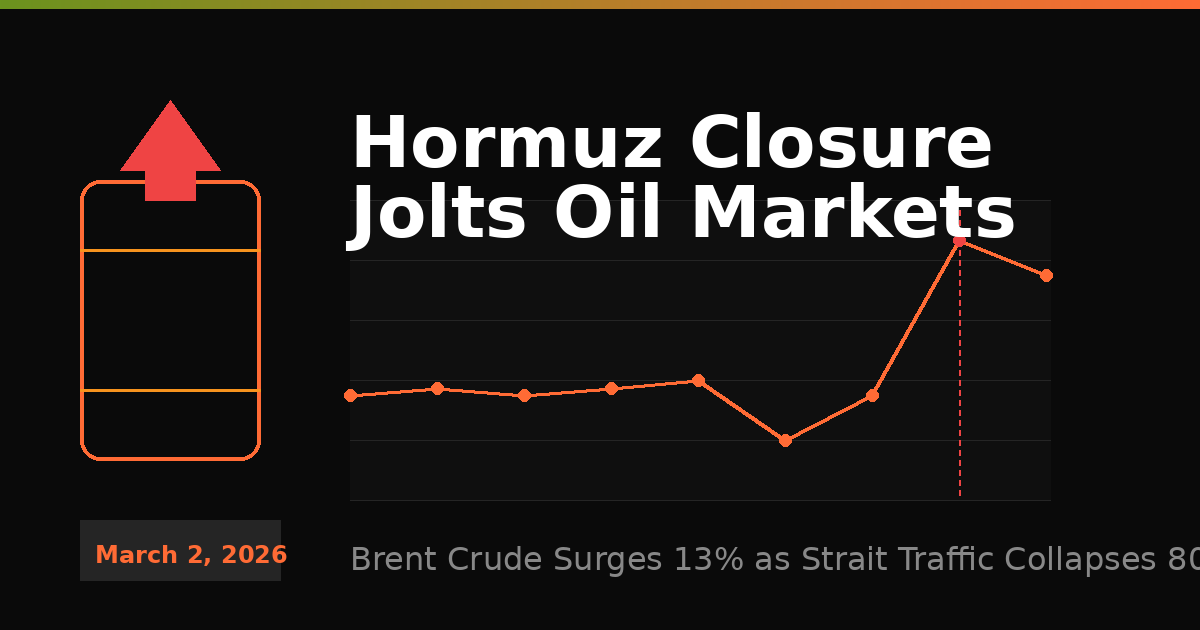

Market Sentiment Tracker: Hormuz Closure Jolts Oil Markets

By Osama on March 3, 2026 in Market Sentiment

Oil prices rose sharply between February 28 and March 2, 2026, following the escalation of military conflict between a U.S.-Israeli coalition and Iran. Brent crude increased from approximately $72 per barrel on February 27 to $82.37 per barrel on March 2, representing an intraday surge of roughly 13 percent. West Texas Intermediate crude followed a similar trajectory, rising from $71 per barrel to $75.33 per barrel over the same period. These price movements reflect market concerns about supply disruptions rather than immediate physical shortages, as global oil inventories remain near historical medians at approximately 74 days of demand coverage.

The primary driver of this volatility is the effective closure of the Strait of Hormuz, which handles approximately 20 percent of global daily oil supply. Shipping traffic through the strait declined by more than 80 percent between March 1 and March 2, with vessel tracking data confirming that tanker transits essentially ceased following Iranian strikes on commercial vessels and energy infrastructure across the Gulf region. Iran's Islamic Revolutionary Guard Corps declared the waterway closed to shipping and threatened to target any vessel attempting passage. War-risk insurance for the corridor was withdrawn over the weekend, which removed the commercial viability of transit even in the absence of direct Iranian interdiction.

%20(1).png)

The broader energy infrastructure in the Gulf has sustained damage that extends beyond shipping disruption. Iranian drone strikes hit Qatar's liquefied natural gas facilities at Ras Laffan and Mesaieed on March 2, forcing QatarEnergy to halt production and declare force majeure on LNG shipments. Saudi Arabia's largest domestic refinery was also shut down following a drone attack. The same geopolitical shock sent European natural gas prices surging 45 percent to €46 per megawatt-hour on March 2, as Qatar's LNG halt combined with Hormuz closure threatened 20 percent of global LNG supply. European gas storage levels already stood below 30 percent capacity, compared to 40 percent in the previous year, leaving the region with minimal buffer against supply interruptions.

The market has embedded a geopolitical risk premium estimated between $4 and $10 per barrel into current prices. This premium reflects the probability-weighted assessment of various scenarios, including a prolonged closure lasting several weeks and the potential for attacks on additional Gulf energy infrastructure. Analysts have suggested that a three- to four-week squeeze on Hormuz traffic could push Brent above $100 per barrel if Gulf producers are forced to curtail output due to the inability to move crude to market.

The timing of this energy shock compounds existing inflationary pressures in the United States. Producer prices rose 0.5 percent in January, with core PPI surging 0.8 percent, both figures exceeding forecasts and maintaining year-over-year growth well above the Federal Reserve's 2 percent target. The oil price surge threatens to add further upward pressure on input costs across manufacturing and transportation sectors, at a moment when U.S. consumer confidence, while improved to 91.2 in February, continues to reflect elevated concerns about prices and inflation. The share of consumers viewing jobs as "hard to get" reached a five-year high at 20.6 percent, suggesting limited wage-driven demand cushion to absorb higher energy costs.

%20(1).png)

China's Leading Economic Index declined in January, adding to concerns about demand from the world's largest crude oil importer. China purchases over 80 percent of Iranian oil and sources roughly 40 percent of its total oil imports through the Strait of Hormuz. While China maintains strategic petroleum reserves that provide short-term coverage, a prolonged disruption would force the country to compete for Atlantic Basin cargoes at elevated prices, tightening global supply further and supporting higher price floors.

%20(1).png)

The strategic implications of this disruption extend beyond immediate price effects. Saudi Arabia and the United Arab Emirates operate bypass pipelines that can redirect some volume away from Hormuz, but these routes do not have sufficient capacity to handle the full export flows of the Gulf producers simultaneously. The current situation is testing whether the global oil market can function effectively when a fifth of daily supply is subject to force majeure and insurance exclusions, even if the physical oil remains producible. The answer will shape energy security planning and risk assessment for the remainder of 2026.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform