Articles

FREE READ: Mapping out the damage to energy infrastructure in latest war

By Osama on March 4, 2026 in Free Articles

.png)

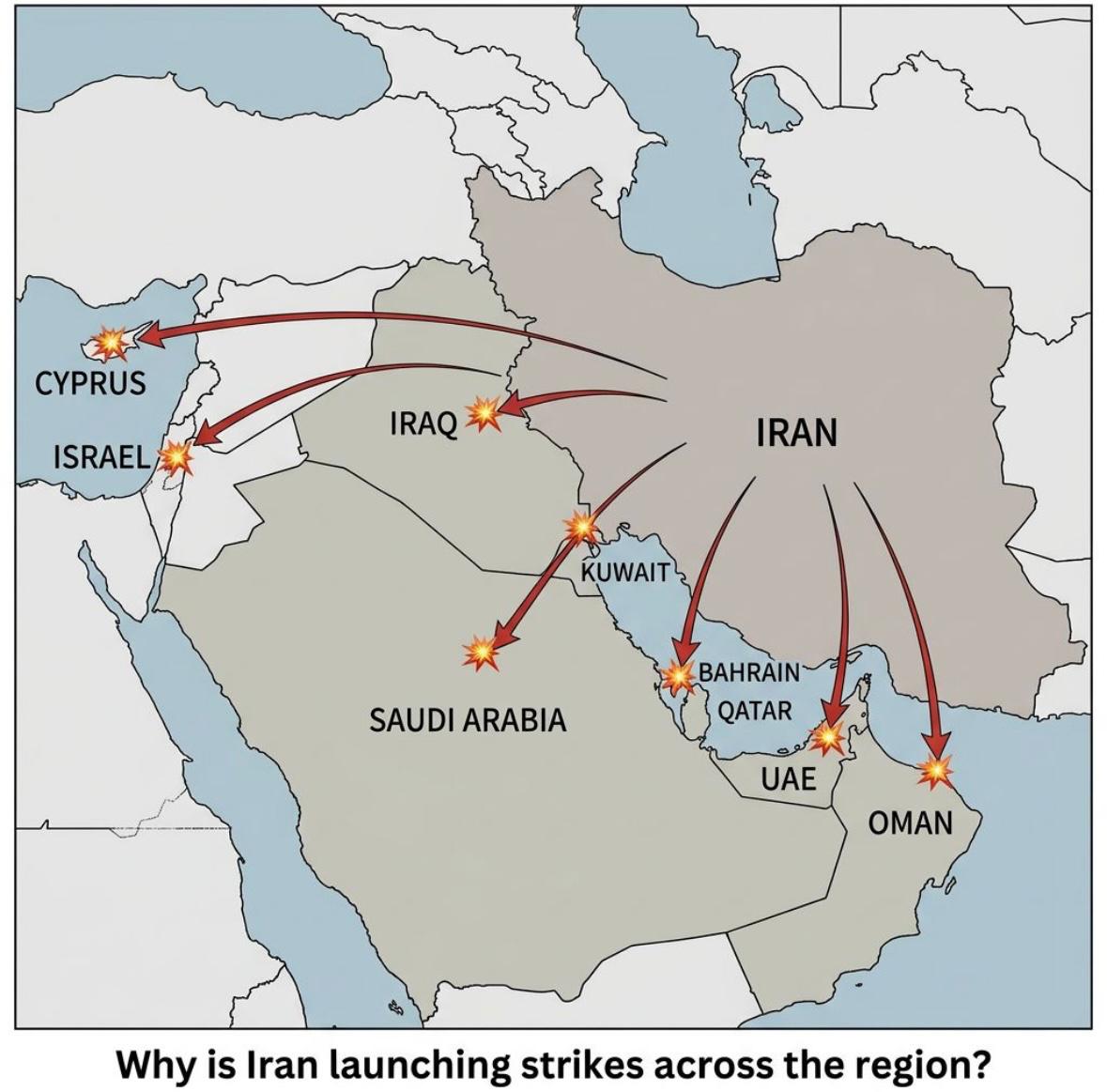

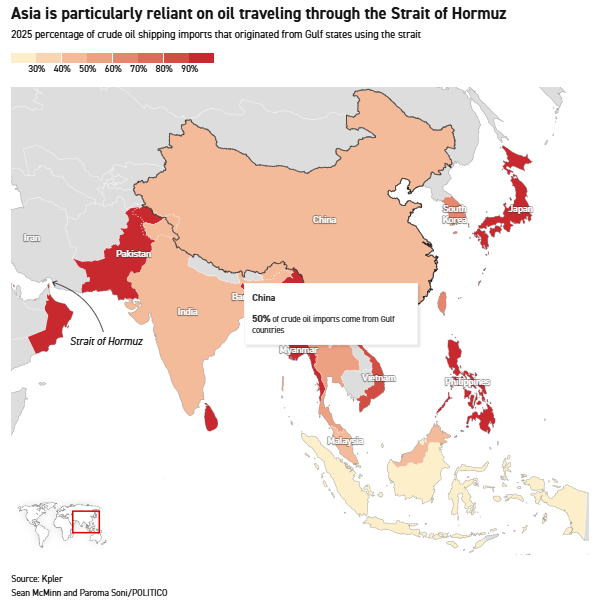

Iran pumps 3.3 million barrels per day of crude plus 1.3 million barrels of condensate, making it OPEC's fourth-largest producer, but the real danger extends beyond domestic production. The country sits on one side of the Strait of Hormuz, a 21-mile-wide waterway through which 20% of the world's crude must pass. When US and Israeli forces struck Iran on February 28, they hit infrastructure critical to Tehran's ability to monetize hydrocarbon reserves. By March 2-3, Iran's retaliatory strikes across the Gulf transformed a targeted operation into a region-wide crisis affecting both oil and gas markets.

Iran's Export Infrastructure Destroyed

The strikes included reported explosions near Kharg Island, Iran's primary offshore export terminal responsible for approximately 90% of the country's crude shipments through the Strait of Hormuz. The facility, which handles an estimated 1.5 million barrels per day — the overwhelming majority destined for Chinese independent refiners, known as "teapots" — represents the single most critical chokepoint in Iran's entire oil export infrastructure.

Strikes hit Bushehr facilities at South Pars, which accounts for roughly two-thirds of Iran's natural gas production, with fires confirmed at Phase 14 and output partially suspended. Additional strikes targeted key refining infrastructure including Abadan, processing over 500,000 barrels daily, alongside Persian Gulf Star and Bandar Abbas facilities along the same vulnerable Gulf coastline. Iran had accelerated tanker liftings ahead of the strikes, moving crude onto the water in anticipation of potential attacks, but Kharg Island — where explosions were confirmed — remains the singular export chokepoint handling 90% of Iran's crude shipments. The full extent of damage to Kharg's loading and storage infrastructure is unconfirmed, but any meaningful degradation of the terminal's capacity would eliminate Iran's ability to reload tankers once floating inventory is consumed, creating a sustained supply shock of over a million barrels daily to Chinese refiners for months.

Iran's Retaliation Hits Regional Energy Infrastructure

Iran's response fundamentally altered the crisis by targeting energy assets across Gulf states. On March 2, QatarEnergy announced a complete halt to LNG production after drone strikes hit facilities at Ras Laffan and Mesaieed. The shutdown removed 20% of global LNG export capacity in a single event, triggering the largest gas price surge since Russia's 2022 invasion of Ukraine.

European wholesale gas prices jumped 52-54% on March 2, with Dutch TTF futures reaching €46 per megawatt-hour. Asian LNG spot prices surged 39%. Qatar supplies major Asian importers including India, China, Japan, and South Korea under long-term contracts, while European buyers rely on Qatari LNG to diversify from Russian pipeline gas.

Simultaneously, Saudi Aramco shut down Ras Tanura refinery after drone strikes. The facility processes 550,000 barrels per day and ranks among the Middle East's largest refineries. Israel also temporarily shut its Leviathan gas field, throttling supply to Egypt and Jordan.

The Strait of Hormuz: The Ultimate Chokepoint

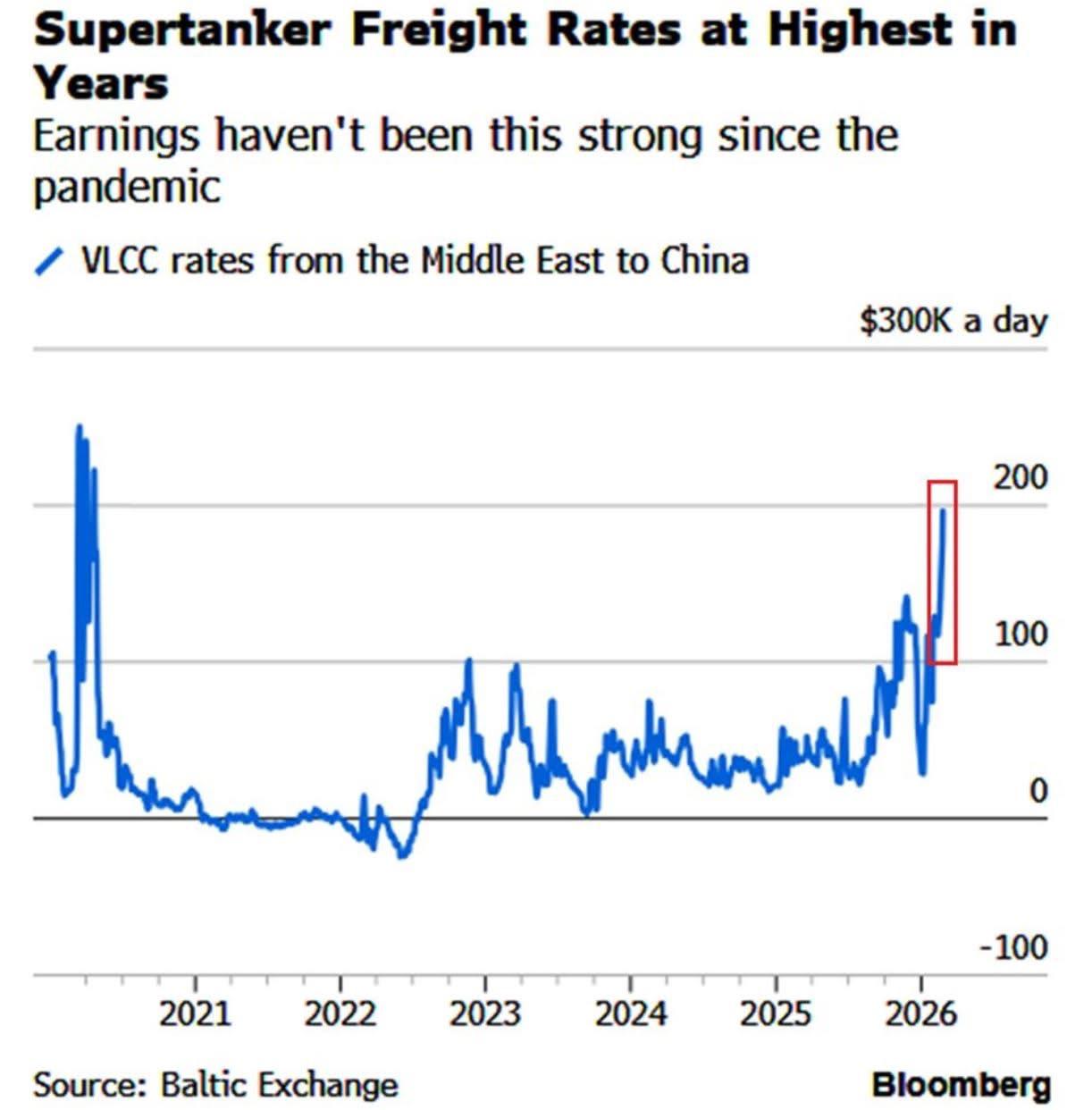

Iran has threatened full closure of the strait. German shipping group Hapag-Lloyd suspended all vessel transit, creating a pileup of approximately 150 freight ships unable to reach Saudi, UAE, Kuwaiti, and Iraqi terminals. War-risk insurance was withdrawn, removing commercial viability of transit. Shipping traffic declined by more than 80% between March 1 and March 2. Approximately 100 vessels now hold position in the Gulf of Oman. The strait handles 13 million barrels per day of crude—31% of all seaborne oil flows—plus substantial LNG volumes.

Market Response and Strategic Implications

Following March 2 escalation, Brent crude surged 13% to $82.37 per barrel—the highest since January 2025. WTI crude jumped 6-12% to $71-75 per barrel. Analysts embedded a $4-10 geopolitical risk premium into current prices. OPEC+ raised production quotas by 220,000 barrels daily on March 1, but capacity only matters if oil can reach refiners. Analysts at JPMorgan suggested a three- to four-week squeeze could push Brent above $100 if Gulf producers cannot move crude to market. The United States maintains a Strategic Petroleum Reserve of 415 million barrels that could dampen spikes, but releases cannot substitute for sustained losses if conflict prevents Gulf exports for months. China maintains reserves providing short-term coverage, but prolonged disruption would force competition for Atlantic Basin cargoes at elevated prices.

Tehran understands its greatest leverage comes from commanding Hormuz and threatening neighbors whose output dwarfs Iran's. Retaliatory strikes across Qatar, UAE, Bahrain, Kuwait, and Saudi Arabia demonstrate that if Iran's revenue is destroyed, the entire Gulf's export capacity becomes a target. The March 2 attacks on Qatar's LNG infrastructure and Saudi Arabia's Ras Tanura refinery show Iran's capability to execute this strategy.

The dual crisis in oil and natural gas markets, combined with maritime insurance withdrawal and Hormuz shipping collapse, creates a perfect storm where each disruption amplifies others. Qatar's LNG shutdown alone threatens energy security for Asian and European buyers dependent on those flows, accounting for significant portions of their import portfolios. European gas storage levels already stood below 30% capacity compared to 40% last year, leaving minimal buffer against supply interruptions. India imported 11.3 million tonnes of Qatari LNG in 2024, while China, Japan, and South Korea maintain long-term contracts now facing force majeure declarations.

Simultaneous constraints on Gulf oil exports through Hormuz multiply the economic and geopolitical stakes beyond any single commodity shock. Saudi Arabia, UAE, Kuwait, and Iraq collectively export several million barrels daily that cannot reach markets if tankers cannot transit the strait. While Saudi Arabia and UAE operate bypass pipelines—the East-West Pipeline to Yanbu and Habshan-Fujairah pipeline to the Gulf of Oman—these routes lack sufficient capacity to handle full export flows simultaneously and were not designed to serve as primary routes under sustained crisis.

Historical precedent offers limited guidance because previous Hormuz threats never materialized into simultaneous attacks on regional energy infrastructure spanning both oil and gas sectors. The 2019 Abqaiq attack removed 7% of global supply temporarily, but shipping continued and Qatar's LNG flowed uninterrupted. The current situation compounds supply loss, shipping paralysis, insurance withdrawal, and infrastructure damage across multiple countries and commodities simultaneously.

If sustained, global markets face their gravest energy shock in decades with consequences extending into recession risk, inflation acceleration, and political instability worldwide. The question is no longer whether prices rise, but whether the global economy can absorb a prolonged disruption to 20% of oil supply and 20% of LNG exports while the world's most critical maritime chokepoint remains effectively closed to commercial traffic.

Tags: