Pressure Pumping Outlook

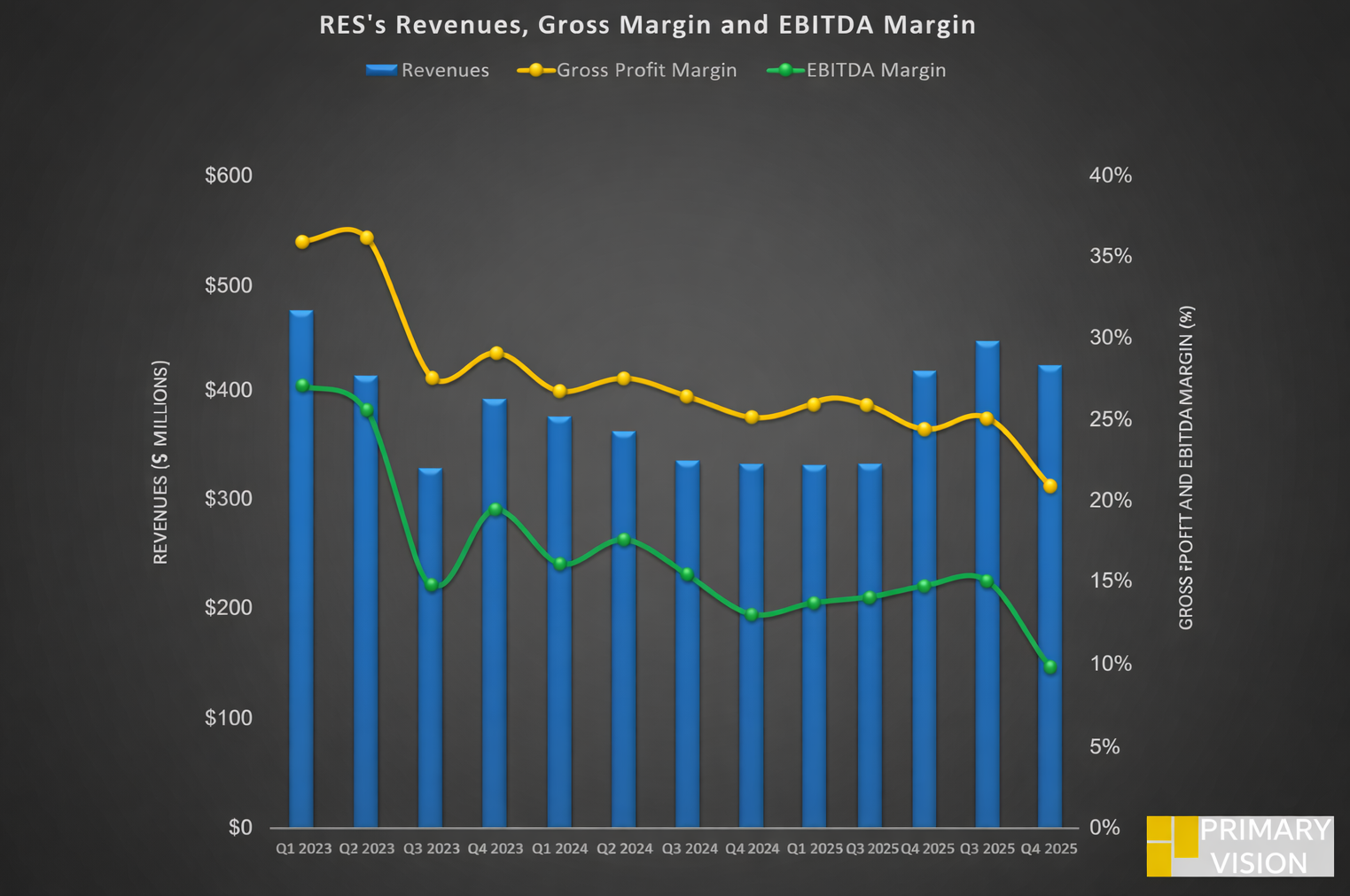

In our recent article, we have already discussed RPC's (RES) Q4 2025 financial performance. Here is an outline of its outlook. RES’s pressure pumping revenue declined 6% sequentially due to holiday downtime and the idling of a frac spread in October. Management does not plan to reactivate that spread until returns improve meaningfully.

Early Q1 activity was also disrupted by winter storms, and the lost operating days will weigh on near-term profitability. Fleet reactivation will depend on both better pricing and confidence in steady programs that can generate incremental cash flow.

Wireline Outlook and Accounting Change

Pintail Completions’ wireline revenue declined 3% in Q4. Here, 2026 activity is expected to closely track large Permian operators. The business remains highly sensitive to completion pacing rather than market share changes.

Beginning in Q4 2025, wireline cables that were previously capitalized and depreciated over 18 months are now expensed due to shorter useful lives from higher activity and changing work types. This accounting change increases cost of revenues and lowers reported EBITDA and capex, but does not affect cash flow.

Thru Tubing Strategies

Thru Tubing Solutions revenue declined 9% sequentially in Q4, with growth in the Southeast and Northeast, flat results in Western Mid-Con, and weakness in international and Rocky Mountain regions. Strategy is centered on technology-led share gains in completions.

The A-10 downhole motor, launched in late 2024, is gaining traction as it addresses longer laterals and higher flow rates. The rollout of the Metal Max power section is expanding reach into new markets by improving torque, reliability, and performance in demanding wells.

Capex Pushback

RES’s FY2025 capex totaled $148 million, which was $12 million lower due to wireline cables being expensed instead of capitalized. About $15 million of the spend was pushed into 2026. As a result, its FY2026 capex is guided at $150–$180 million and will flex with activity levels.

Relative Valuation

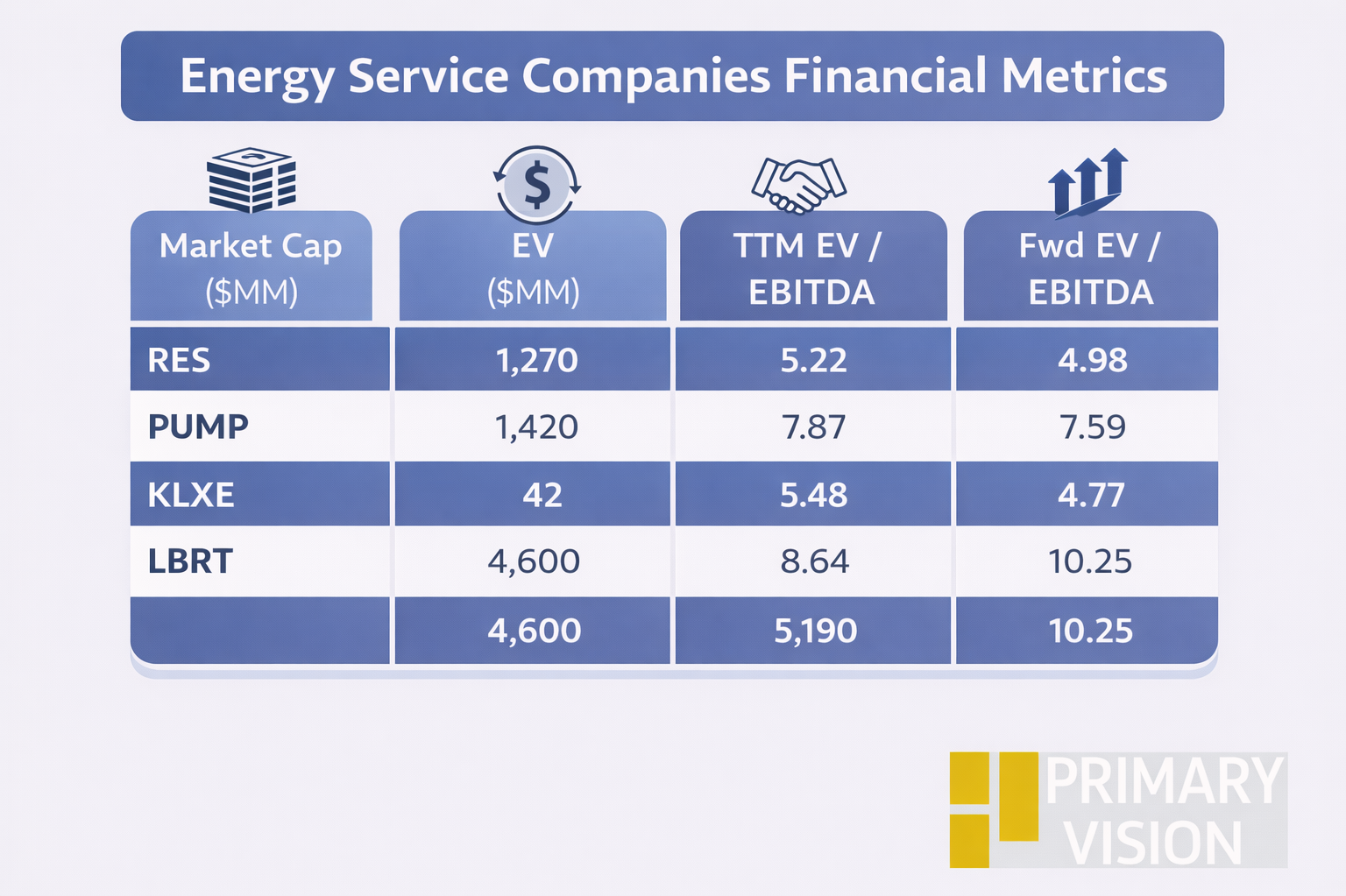

RES is currently trading at an EV/EBITDA multiple of 5.2x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is ~5x. The current multiple is significantly lower than its five-year average EV/EBITDA multiple of 13.6x.

RES's forward EV/EBITDA multiple is expected to contract more steeply than its peers. This implies that the company's EBITDA is expected to increase more sharply than its peers in the next four quarters. This typically results in a higher EV/EBITDA multiple. The stock's EV/EBITDA multiple is slightly lower than its peers' (PUMP, KLXE, and LBRT) average of 7.3x. So, the stock appears undervalued compared to its peers.

Final Commentary

RPC’s near-term conditions remain pressured, with weaker pressure pumping activity, weather disruptions, and no urgency to reactivate idled fleets without better pricing and cash returns. Wireline performance is tied closely to Permian completion pacing, while an accounting change weighs on reported margins but not underlying cash flow.

Thru Tubing is using differentiated tools to defend and grow share despite regional softness. Capital spending is being deferred and kept flexible as management prioritizes returns over volume. Overall, RES is staying disciplined through the downturn while positioning for improvement when pricing and activity stabilize. The stock appears undervalued compared to its peers.