Articles

- BLOG / Articles / View

- Articles

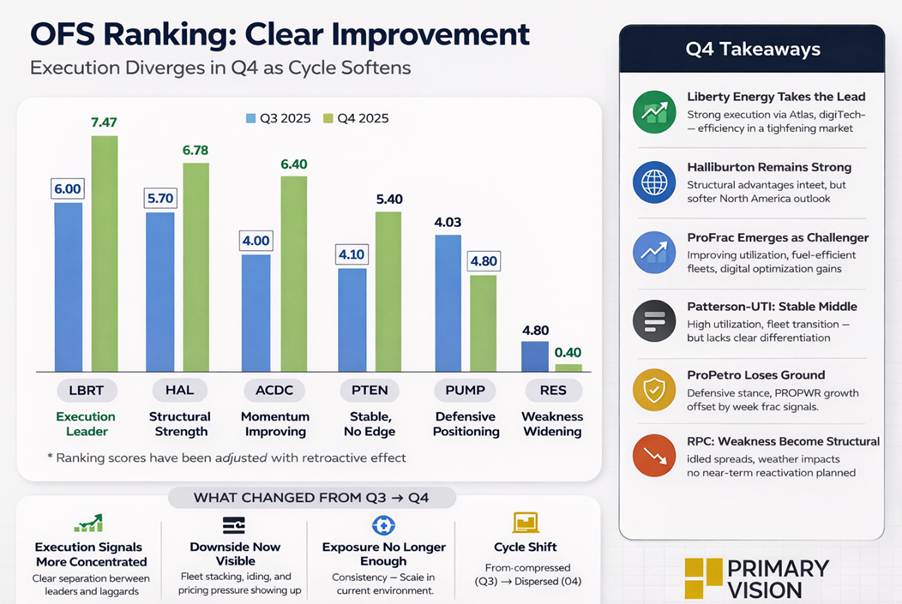

Pressure Pumping Ranking in Q4: Execution Diverges As Cycle Softens

By Avik on March 25, 2026 in Articles

Ranking Pressure Pumpers in Q4

This analysis evaluates Halliburton, Liberty Energy, Patterson-UTI, ProPetro, RPC, and ProFrac using the same framework outlined previously. The focus remains on how effectively companies convert completion activity into operational performance.

The Q4 update reflects a more dispersed environment. In our previous ranking article in Q3’25, rankings were tightly clustered, supported by relatively stable activity. In Q4, execution differences are clearer, and the gap between operators is widening.

Liberty Energy: Execution Moves to the Front

Liberty moves into the top position, driven by a cleaner execution profile. Management continues to emphasize completion intensity, real-time optimization, and continuous pumping, supported by Atlas and digiTechnologies. These initiatives are directly tied to improving fleet utilization and operational decision-making in a tighter market.

At the same time, equipment attrition and underinvestment are reducing available frac capacity. In this environment, efficiency becomes more valuable than scale. Liberty’s ability to maintain consistent execution under these conditions gives it an edge. The result is not a step-change in activity, but a more reliable operating profile. That is enough to move it ahead.

Halliburton: Strong Position, More Balanced Signals

Halliburton remains near the top, supported by its scale, technology, and international exposure. However, Q4 signals reflect a softer near-term environment. Management is guiding to high-single-digit declines in North America, continued fleet stacking, and margin pressure in completions.

The company is responding by prioritizing returns and leaning on differentiated technologies such as ZEUS, iCruise, and LOGIX. These continue to support performance, particularly as well complexity increases. Halliburton’s positioning remains strong. But compared to Liberty, the execution signals are more mixed, which narrows its lead.

ProFrac: Execution Momentum Builds

ProFrac stands out as the most notable mover in Q4. Management highlights stable pricing, improving utilization, and stronger operational efficiency, supported by its vertically integrated model and fuel-efficient fleets.

Rising diesel costs are increasing the value of dual-fuel and electric fleets, strengthening ProFrac’s positioning. At the same time, investments in closed-loop fracturing and digital optimization are beginning to translate into more consistent execution. This is not a scale story. It is an execution story. ProFrac is performing better in a weak market, and the ranking reflects that shift.

Patterson-UTI: Stable, but Lacking Differentiation

Patterson-UTI remains in the middle of the group, with a largely unchanged profile. The company continues to operate with high utilization and minimal spare capacity while shifting toward natural gas-powered fleets and digital completions.

These moves improve long-term asset quality. However, the near-term signal profile remains balanced. There is no clear deterioration, but also no strong improvement. In a cycle where execution is becoming the key differentiator, that leaves Patterson-UTI without a clear path to move higher.

ProPetro: Discipline, but Limited Upside in Frac

ProPetro slips in the rankings as execution signals weaken. Management continues to emphasize pricing discipline, contracted fleets, and capital allocation toward electrification and automation.

These are constructive steps, but they are largely defensive. The focus is on protecting margins rather than improving utilization or expanding activity. PROPWR is emerging as a meaningful growth driver, but that sits outside core pressure pumping execution. Within frac, the signal profile lacks strong positives. In Q3, stability was enough. In Q4, it is not.

RPC: Weakness Becomes More Visible

RPC remains at the bottom, with a widening gap. The company idled a frac spread in October and does not plan to reactivate it without meaningful pricing improvement. Activity remains sensitive to weather and customer pacing, while revenue and margins are under pressure. Management is maintaining discipline, but the signal profile reflects a business responding to conditions rather than driving them. As the cycle softens, that difference becomes more pronounced.

What Changed From Q3

The shift from Q3 to Q4 is driven by execution, not activity. In Q3, stable conditions allowed most operators to cluster together. Execution differences existed, but they were not decisive. In Q4, those differences become clearer.

Execution signals are now more concentrated. Liberty and ProFrac show stronger consistency, while Halliburton remains solid but more balanced. The rest of the group shows increasing signs of pressure. At the same time, the downside is becoming more visible. Fleet stacking, idling decisions, pricing pressure, and cost challenges are now showing up more clearly in management commentary. Exposure still matters, but it no longer drives rankings on its own. Execution under tighter conditions is now the primary differentiator.

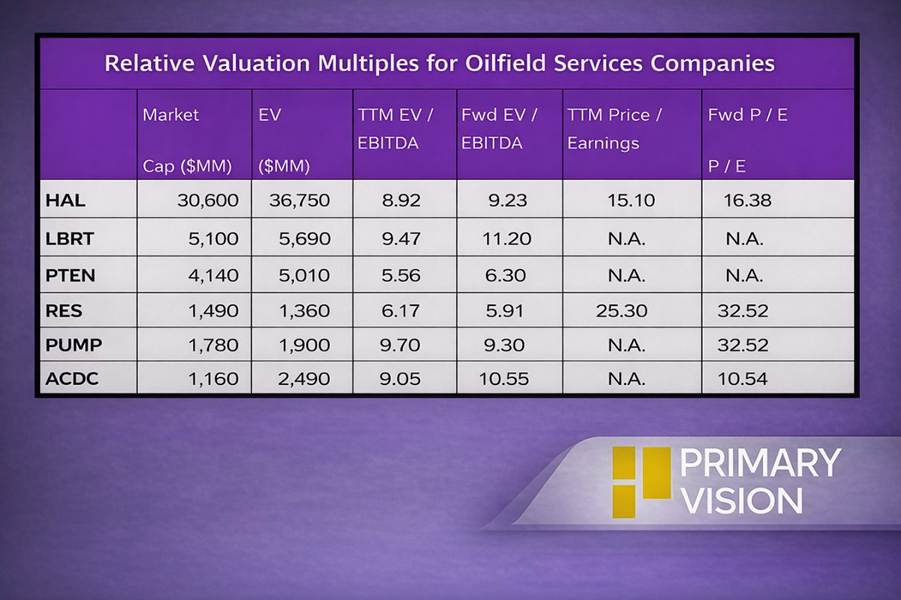

Relative Valuation: What’s Cheap; What’s Not?

Based on changes in relative valuation multiples (EV/EBITDA), RES appears attractively priced, with low trading multiples. LBRT, PUMP, and ACDC, based on the relative valuation multiples, are the least attractively placed. HAL and PTEN are reasonably spread across the pricing spectrum.

Takeaway

The Q4 update marks a transition in the cycle. Leadership is shifting toward companies that can maintain consistent execution in a softer market. Liberty now leads on that metric. Halliburton remains close behind but with a more balanced outlook. ProFrac is improving and gaining ground.

Mid-tier players are losing relative positioning, and RPC’s weakness is becoming more structural. As completion activity stabilizes, the gap between operators is widening. The ranking is now reflecting that reality more clearly.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform