Articles

- BLOG / Articles / View

- Articles

Gas Resilience Is Rewriting the U.S. Shale Playbook

By Avik on March 20, 2026 in Articles

Gas Supply Shows Unexpected Resilience in the Shale Patch

The U.S. shale sector is entering a phase where production is no longer highly responsive to short-term commodity price movements. Data from producers and oilfield service companies suggests that natural gas supply, in particular, has become structurally resilient despite a sharp decline in prices. Here, we evaluate the US shale scenarios at the end of 2025, going into 2026.

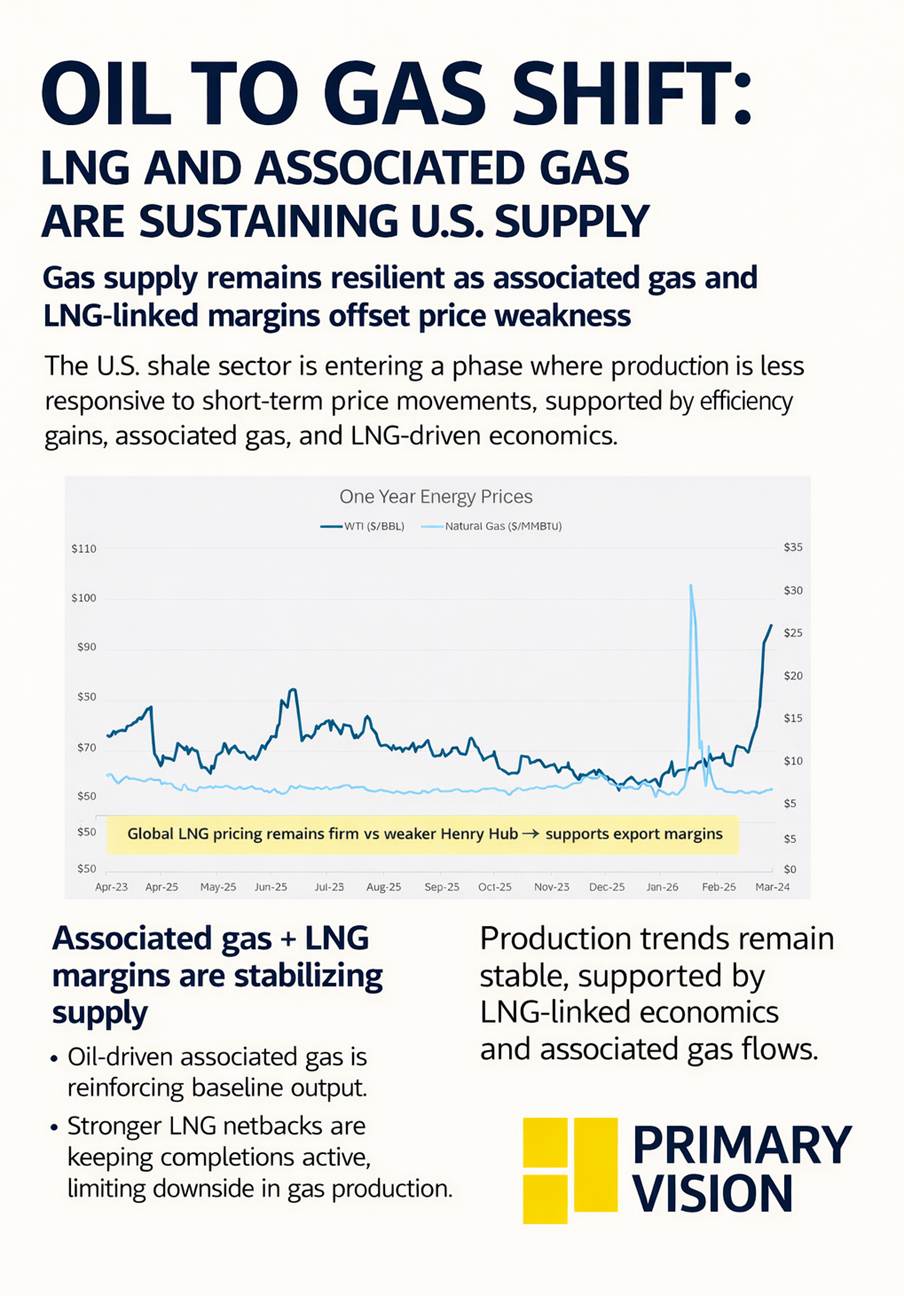

The contrast between commodity prices and production trends in 2025 highlights this shift. Henry Hub natural gas prices fell roughly 26% year over year, declining from about $3.50/MMBtu in 2024 to around $2.60. Oil prices were far more stable, with WTI declining only about 6% from roughly $80 per barrel to $75. Yet the production response was surprisingly muted.

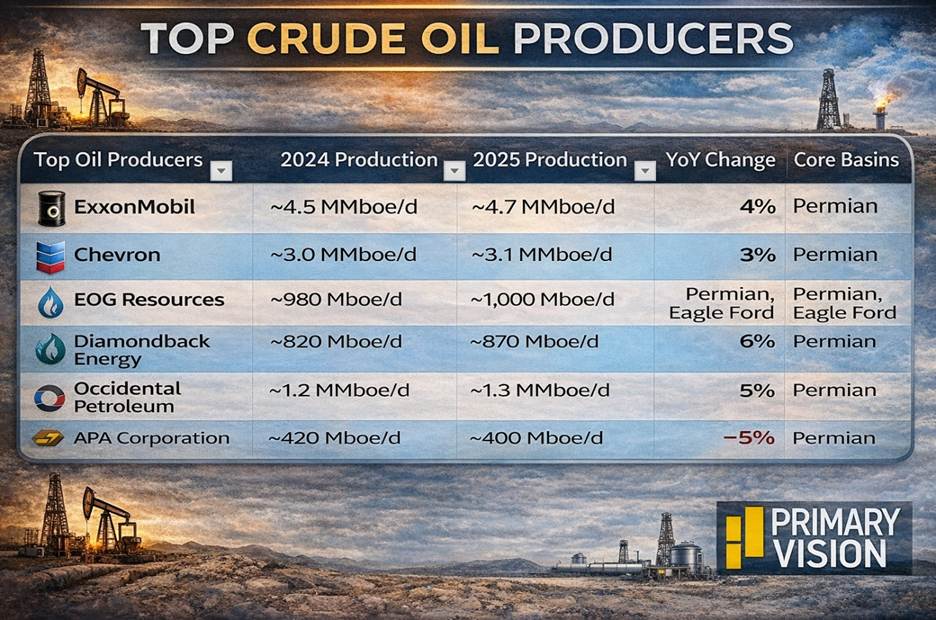

On average, oil-weighted producers increased output by roughly 2.5%, supported by continued activity in the Permian Basin and ongoing efficiency gains.

Gas-Focused Producers Show Limited Declines

Gas-focused producers exhibited only minor production changes despite the much sharper price decline.

Average production for the gas-focused group declined by only about 1%, indicating a muted supply response relative to the magnitude of the price shock.

Efficiency Gains Are Changing the Supply Response

The disconnect between lower activity and stable production reflects continued efficiency improvements in shale development.

Producers are drilling longer horizontal laterals and increasing completion intensity, allowing more reservoir exposure per well. Companies such as EOG Resources now routinely drill multi-mile laterals in several plays, significantly increasing production per well.

These gains allow operators to sustain production with fewer wells, reducing the direct link between drilling activity and output. At the same time, rising diesel costs are increasing the importance of fuel-efficient frac fleets, further reinforcing capital discipline and operational efficiency across the sector.

Associated Gas and LNG Are Reinforcing Supply

A key factor behind gas supply resilience is the growing role of associated gas from oil drilling. The second factor is US’s LNG exports.

Among the oil-focused producers analyzed, natural gas accounts for roughly 39% of total production on average. This means a substantial portion of the U.S. gas supply is tied to oil-directed activity rather than standalone gas economics. As long as oil production continues in the Permian Basin, associated gas volumes will continue to grow, regardless of short-term gas price movements.

Gas production’ stickiness shows that economics are increasingly tied to global LNG markets rather than domestic benchmarks. I think the widening spread between weaker U.S. gas prices and firmer LNG prices has preserved export netbacks, even after accounting for liquefaction and shipping costs. This allows producers, marketers, and refiners to share in LNG-linked margins, which in turn keeps completion activity more resilient than headline pricing would imply. Oil output continues to grow modestly, but it is this LNG-driven support—along with associated gas—that is preventing a sharper contraction in overall gas supply.

Service-Sector Signals Point to Constrained Activity

Oilfield service data confirms that operators did reduce activity. Pressure-pumping companies reported weaker completion demand through 2025, with declining frac fleet utilization and selective idling of equipment. RPC, for example, disclosed that it idled a frac spread in October due to weaker returns.

However, recent commentary from ProFrac suggests that activity is not simply falling but being restructured. Operators are pulling forward DUC completions and tightening completion schedules, leading to denser activity periods without a corresponding increase in overall drilling intensity.

At the same time, limited new frac capacity and ongoing equipment attrition are beginning to constrain supply in the pressure-pumping market. This reduces the ability of operators to rapidly scale activity even if prices improve.

The Emerging Structure of Shale Supply

Taken together, these trends suggest the U.S. shale system has become structurally less responsive to commodity price swings. Oil producers continue to deliver modest growth, while gas producers maintain relatively stable output despite significant price declines. Meanwhile, associated gas from oil drilling reinforces overall supply.

The result is a system that adjusts gradually rather than rapidly to price signals. As LNG demand expands later this decade, this structural resilience could play a critical role in shaping U.S. natural gas markets. Instead of sharp supply responses to price movements, shale production may increasingly evolve within a more constrained and efficiency-driven framework.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform