Outlook & Key Projects: ProPetro’s completions outlook is turning constructive. Management highlighted early signs of recovery, with activity and pricing benefiting from a stronger commodity backdrop and structurally tight frac supply following industry attrition. Frac spread count is expected to increase to ~12 active spreads in Q2, indicating a recovery from Q1 weather disruptions and improved demand visibility.

PROPWR remains the central growth vector and the key project focus this quarter. The strategic framework agreement with Caterpillar materially expands long-term capacity visibility, adding ~2.1 GW and bringing total potential capacity to ~2.6 GW by 2031. Commercial traction is accelerating. The company is in advanced negotiations for ~100 MW of oil and gas microgrid deployments, while also progressing several hundred megawatts of data center opportunities.

Q1 Performance

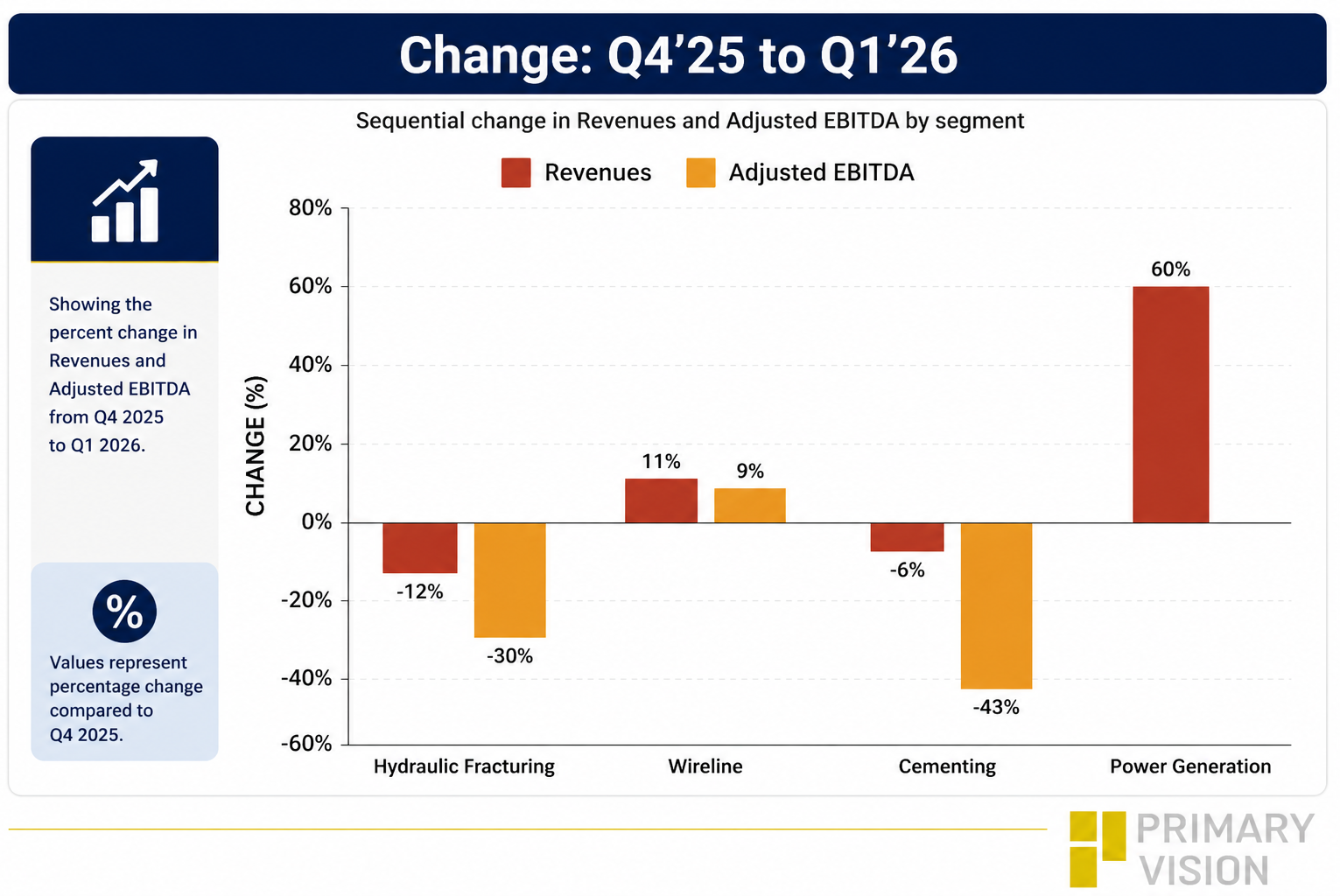

Revenue declined ~7% QoQ in Q1 2026, reflecting lower completions activity driven by adverse weather and reduced utilization. Adjusted EBITDA declined ~26% QoQ, with margins compressing to 13%, highlighting the operating leverage inherent in the completions business during activity downturns.

Hydraulic fracturing was the primary driver of the decline, with both revenue and EBITDA falling sequentially as utilization dropped. Wireline was relatively stable, while cementing saw modest softness, reflecting broader completions slowdown. PROPWR continues to scale but remains a drag on consolidated profitability in the near term, as investments ramp ahead of revenue contribution.

Cash Flows and Capex Guidance: Operating cash flow declined sharply in Q1, driven by lower EBITDA and working capital outflows. FY2026 capex is guided to $540M–$610M, up ~100% from $281 million in FY2025, reflecting a step-change in PROPWR investment. The majority of this is allocated to PROPWR, underscoring the scale of investment behind the platform.

Importantly, a significant portion of PROPWR capex is expected to be financed, reducing near-term cash burden while enabling growth. Liquidity remains solid at ~$289 million, providing flexibility to fund both completion operations and PROPWR expansion.

Thanks for reading the PUMP Take Three, designed to give you three critical takeaways from PUMP's earnings report. Soon, we will present a second update on PUMP earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.