Articles

- BLOG / Articles / View

- Articles

Market Sentiment Tracker: What Do Rising Bond Yields Mean?

By Osama on May 19, 2026 in Market Sentiment

Something broke in the sovereign bond market this week, and it broke everywhere at once. US 30-year above 5%, UK gilts jumping 42 basis points, JGBs pushing toward levels that make Japan's debt arithmetic frightening. The market has abandoned the assumption that central banks will rescue duration holders anytime soon — and the repricing is just getting started.

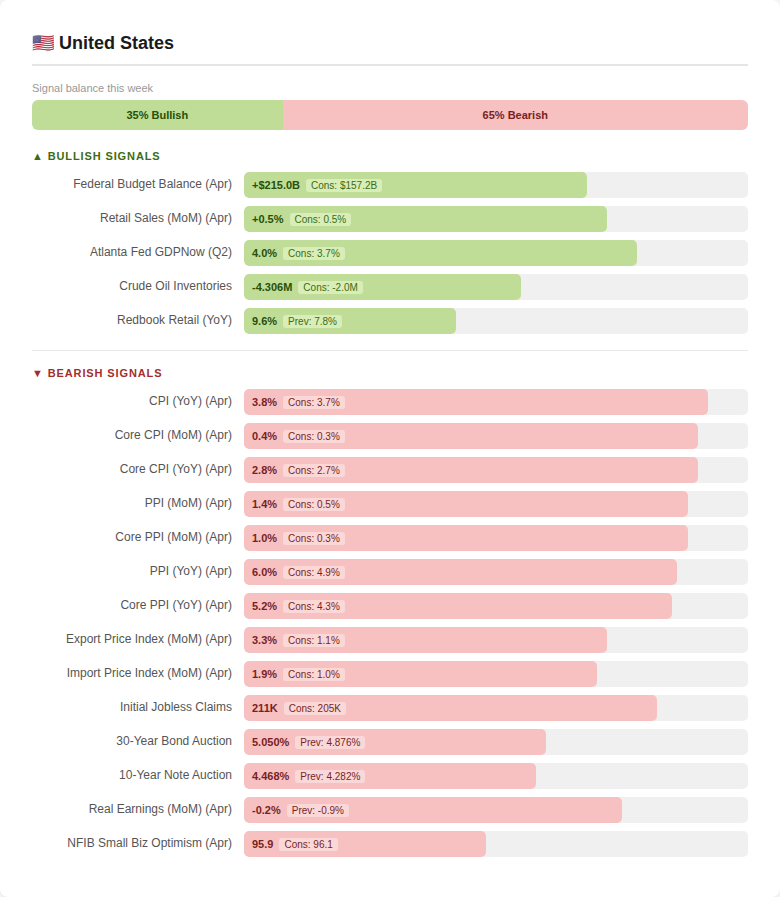

🇺🇸 United States

The 30-year clearing at 5.05% and the 10-year at 4.47% aren't just higher numbers — they're the bond market telling you the policy regime has changed. For most of the past year, the long end was willing to sit tight on the assumption that rate cuts were coming. That assumption is now being unwound, and the repricing has legs. With producer costs running nearly triple consensus and the tariff pipeline still pushing upstream inflation toward the consumer, there's no credible path to easing before 2027. The term premium is back, and it's demanding real compensation for duration risk.

What makes this dangerous is the fiscal backdrop. The April budget surplus of $215 billion looks healthy on the surface, but it's seasonal — tax receipts always spike in April. The structural deficit hasn't changed, and Washington is still issuing at a pace that requires the market to absorb massive supply at these elevated yields. Every 10-year auction that clears above 4.4% raises the cost of rolling existing debt. The 52-week bill came in at 3.65%, up from 3.49% — even the front end is creeping higher. We're entering a reflexive loop where higher yields increase the deficit, which increases issuance, which pushes yields higher still. The Fed can hold rates steady and the fiscal math alone does the tightening for them.

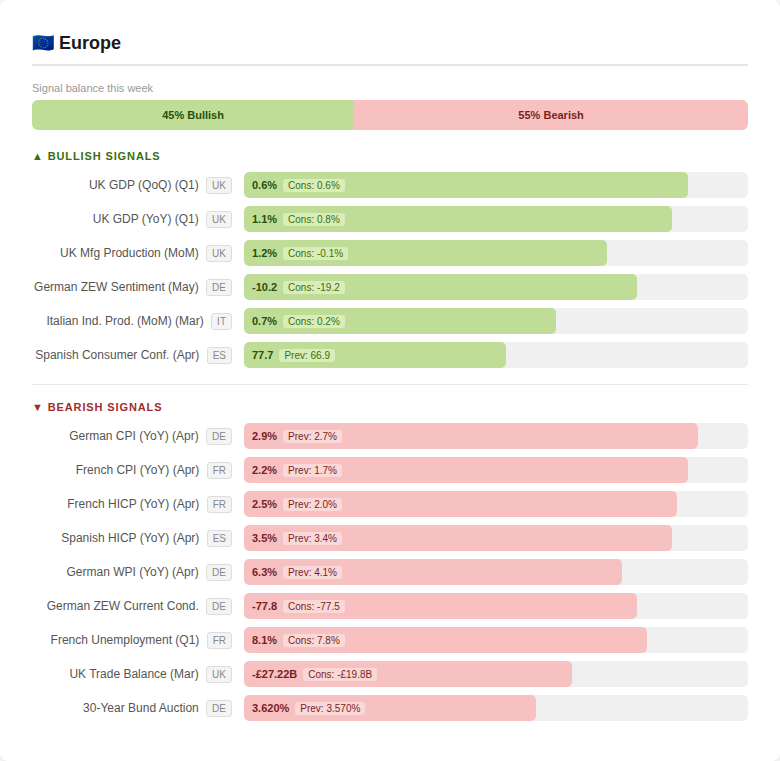

🇪🇺 Europe

The same dynamic is playing out across the Atlantic, just with a slightly different accent. The German 2-year Schatz auctioned at 2.70%, up sharply from 2.47%. The 30-year Bund cleared at 3.62%, versus 3.57% prior. The UK 5-year gilt came in at 4.65%, a full 42 basis points above the previous auction. These aren't marginal moves — they represent a coordinated repricing of sovereign risk across every major European issuer in a single week.

The trigger is identical to the US: inflation refusing to cooperate. When every major eurozone economy prints hotter than the month before, the market stops waiting for central bank guidance and starts pricing the world as it is. The ECB's June meeting is now a non-event — nobody expects a cut, and the conversation has shifted to how long the hold lasts. But Europe has a problem the US doesn't: fragmentation risk. Italian 3-year BTPs cleared at 2.98% and 7-year at 3.55% — both higher — and unlike Germany, Rome doesn't have the fiscal space to absorb persistently elevated borrowing costs. The spread compression trade that worked through 2024 and 2025 is starting to look vulnerable. If Bund yields keep rising and pull peripheral spreads wider, the ECB will face the same tension that nearly broke the eurozone in 2022: fighting inflation while preventing a sovereign stress event in the south.

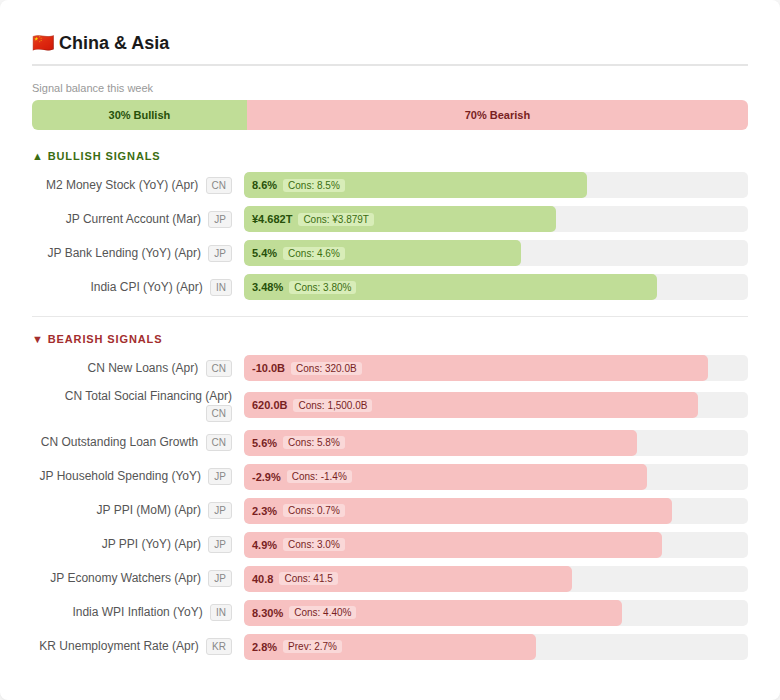

🇨🇳 China & Asia

Japan is the clearest expression of the global yield problem — and the most fragile. The 10-year JGB auctioned at 2.54%, up from 2.35%, and the 30-year at 3.84%, up from 3.70%. For a country carrying a debt-to-GDP ratio above 250%, these moves matter far more than they would elsewhere. Every basis point costs Tokyo exponentially more than it costs Washington or Berlin. The BoJ has been gradually stepping back from yield curve control, but the market is now testing how far that retreat goes. If JGB yields continue climbing at this pace, debt servicing costs start crowding out everything else in the budget within quarters, not years.

The broader Asian picture compounds this. Beijing can't generate credit demand despite abundant liquidity — loan creation went negative while social financing collapsed to a fraction of expectations. That means China won't be exporting growth to the region anytime soon. Meanwhile, India's wholesale inflation nearly doubled consensus, driven by a fuel cost shock that directly raises the government's subsidy burden and borrowing needs. The global yield surge is creating a feedback loop across Asia: higher US rates strengthen the dollar, weaken Asian currencies, raise import costs, force tighter domestic policy, and choke the very growth that would make the debt sustainable. Every central bank in the region is watching the US 10-year more closely than their own data right now — because that's the rate that actually sets their policy constraint.

Watch three tripwires over the coming quarter. The 10-year JGB pushing through 2.7% without BoJ intervention — that triggers forced selling from Japanese institutions into global markets. The BTP-Bund spread widening past 200 basis points — that forces the ECB into a credibility-destroying choice. And in Washington, the reflexive loop between deficit issuance and rising borrowing costs has no circuit breaker short of a recession. The next leg of this move won't come from inflation data. It'll come from a fiscal accident

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform