Articles

- BLOG / Articles / View

- Articles

Market Sentiment Tracker: Tariffs overruled, hiring and uncertainty

By Osama on May 12, 2026 in Market Sentiment

The week's data arrived against a backdrop that keeps shifting underfoot. The Supreme Court struck down IEEPA tariffs in February, the Court of International Trade invalidated the Section 122 replacements on May 7, and the Trump-Xi summit is days away. Markets are treating all of this as progress toward normalization. The macro data says the damage is already embedded.

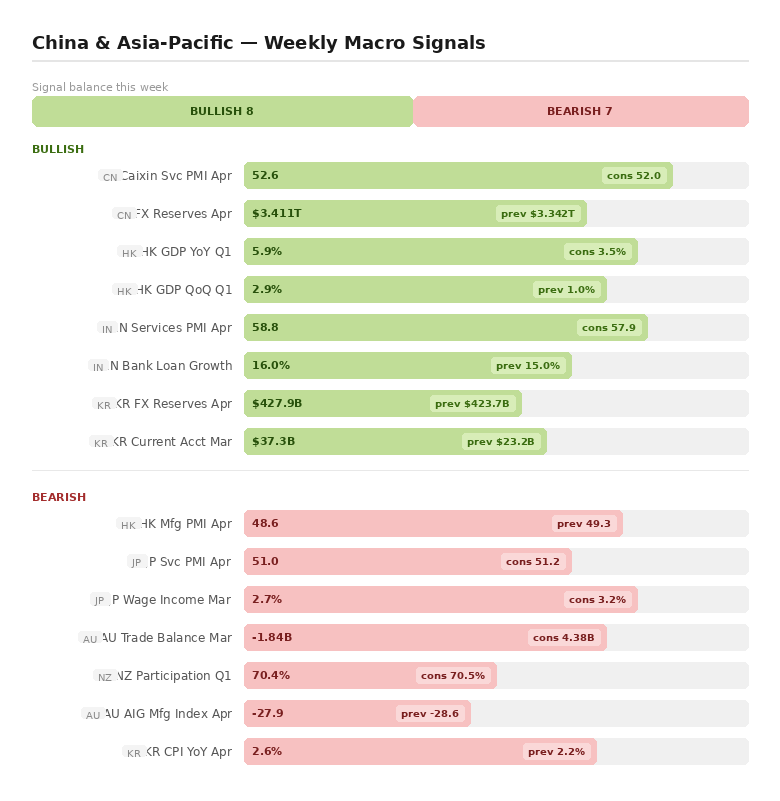

In the US, nonfarm payrolls printed 115K against a consensus of 65K, and that number is going to dominate the narrative in ways that obscure what actually happened. The beat was almost entirely private-sector services hiring — manufacturing shed 2K jobs when the street expected gains of 5K, and government payrolls contracted by 8K. Average hourly earnings rose just 0.2% month-over-month, a tenth below forecast, and average weekly hours ticked to 34.3. So the labor market is adding positions, but those positions carry less income per hour and fewer hours per week than what they're replacing. The consumer credit report tells you how households are responding to that squeeze: $24.86B in new credit against expectations of $12.5B, nearly double. That's not confidence — that's compensation. When income growth stalls and spending doesn't, the gap gets financed. The ISM services PMI held at 53.6, close enough to consensus to look stable, but new orders collapsed from 60.6 to 53.5 in a single month. That's the sharpest one-month decline in the forward pipeline since early 2024, and it lands alongside Challenger job cuts jumping to 83.4K from 60.6K. Firms haven't started firing in scale yet, but the announcements are accelerating. The Atlanta Fed's GDPNow still reads 3.7% for Q2, and that number is real — but it's being sustained by credit-financed consumption, not by broadening income growth. That distinction is what separates a durable expansion from one that's running on fumes.

.png)

The connection to Europe runs through the trade channel, and what's happening there is more alarming than anything in the US data. The eurozone services PMI fell from 50.2 to 47.4 in April — a drop that S&P Global noted produced the sharpest decline in new business since October 2023 and pushed input cost inflation to a 40-month high. That combination is stagflationary: demand is contracting while costs are rising, which means firms can't pass through prices and can't cut them either. Germany's services PMI dropped from 50.9 to 46.9. France fell to 46.5. Spain — which had been the bright spot holding above 50 through most of the post-tariff adjustment — collapsed to 47.9, missing consensus by four full points. This is no longer a manufacturing recession leaking into services at the edges. The eurozone's service sector, which is roughly 70% of GDP, is now contracting simultaneously across the three largest continental economies. Germany's factory orders surging 5.0% against a 1.0% consensus might look like a counterweight, but industrial production fell 0.7% in the same month. Orders are accumulating that aren't being fulfilled — which means firms are either facing supply constraints from the ongoing Middle East disruption to logistics or, more likely, they don't trust the orders to hold and aren't investing to meet them. The UK's services PMI at 52.7 is genuine outperformance, but UK construction PMI at 39.7 — missing consensus by six points — shows that housing and commercial development have effectively stalled. The ECB is now watching a synchronized services contraction while dealing with accelerating cost pressures and a French budget deficit that widened to -42.9B. The policy response available is narrow: rate cuts risk amplifying already-rising input costs, and fiscal stimulus is constitutionally constrained in Germany and politically fraught in France.

.png)

And then there's Asia, where the data looks superficially stronger but the strategic subtext matters more than the prints. China's FX reserves jumped $69 billion to $3.411 trillion in a single month. For context, reserves grew by only $160 billion across all of 2025 despite a record $1.19 trillion trade surplus — most of that surplus never came home. This month's accumulation is a different kind of move. With the Trump-Xi summit approaching, the tariff legal framework in chaos after the CIT ruling, and Beijing having already slashed tariffs on 935 strategic import categories to fortify its high-tech supply chains, this reserve build looks like preparation for renewed volatility rather than passive accumulation. The Caixin services PMI at 52.6 confirms that domestic consumption continues recovering, but the pace is incremental, and Hong Kong's manufacturing PMI at 48.6 shows the trade transmission channel remains broken. Hong Kong's 5.9% Q1 GDP — beating consensus of 3.5% — is almost certainly inflated by front-loaded shipments ahead of tariff uncertainty; that activity was pulled forward from mid-year and won't repeat. Japan's wage growth printing 2.7% against 3.2% expectations is quietly consequential: the BoJ's entire rate normalization thesis depends on wages sustaining above 3%, and this is the second consecutive miss. If wage growth doesn't re-accelerate, the yen stays weak, which creates competitive pressure across the rest of Asia and complicates India's otherwise strong position.

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform