Articles

Free Read: Refiners Are Prioritizing Jet Fuel Over Gasoline

By Osama on May 21, 2026 in Free Articles

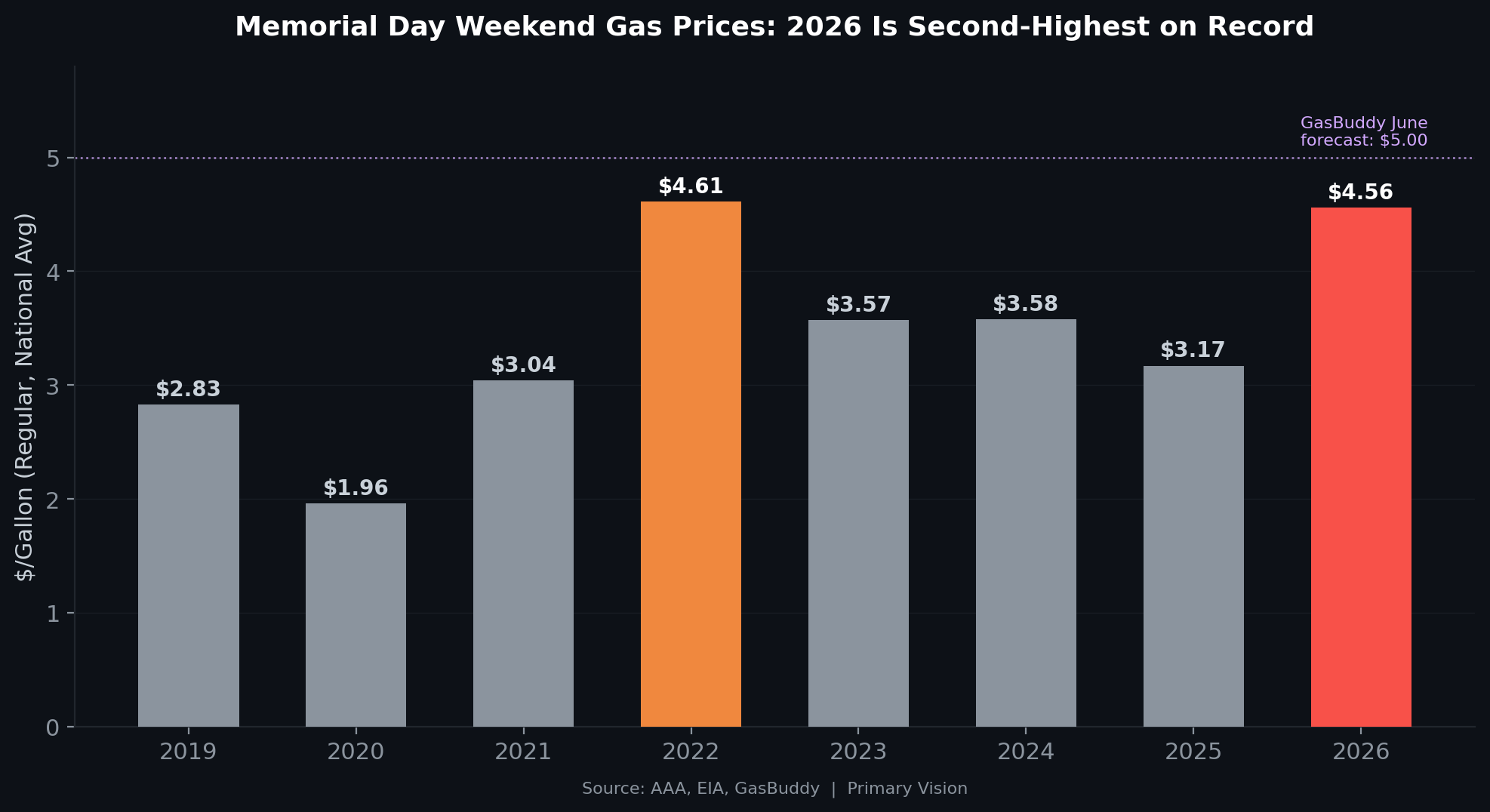

Memorial Day is four days out. A record 39.1 million Americans are expected to drive somewhere this weekend, and they'll be paying $4.56 a gallon on average to do it — the most expensive fill-up since 2022. GasBuddy is calling for $4.80 as a summer average, with $5 a real possibility next month if Hormuz stays shut. Gas is now above $4 in all 50 states. California is at $6.15.

And yet — people are still driving. That's the part worth paying attention to.

Gasoline product supplied — the EIA's demand proxy — averaged 9.0 million barrels a day over the last four weeks, up 1% year-over-year. At these prices, the playbook from 2022 said demand destruction should be biting. It isn't. Not yet, anyway. The consumer is absorbing $4.50 gasoline the way they absorbed $4 gasoline last cycle — grumbling about it but still filling up. The question is whether $5 is the line. GasBuddy's Patrick De Haan thinks it might take closer to $6 for the real behavioral shift to kick in.

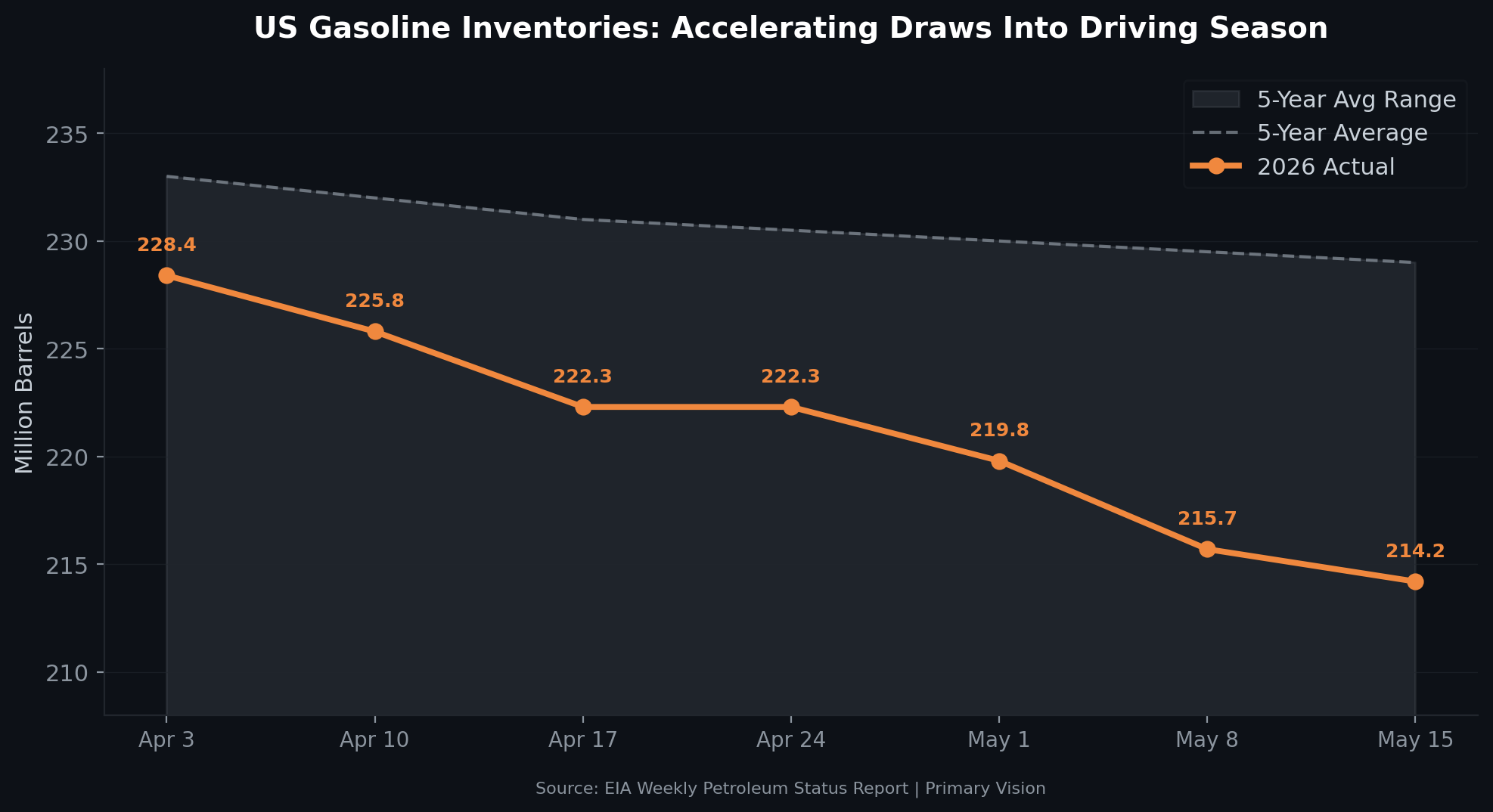

Meanwhile, gasoline inventories are not in a good place. Stocks fell to 214.2 million barrels as of May 15 — down from 222.3 million just three weeks earlier. The five-year average heading into this weekend is comfortably above 230 million. We're walking into the highest-consumption stretch of the year running well below seasonal norms, and the draw is accelerating.

So where's the gasoline going to come from? That's where this gets interesting — because the refining system is being asked to do two things at once, and it can't fully deliver on both.

On the other side of the Atlantic, the jet fuel picture is genuinely scary. The Hormuz closure didn't just pull crude off the water — it blew a 400,000-barrel-a-day hole in the global jet fuel trade, roughly 20% of world supply. Europe is now weeks away from what Goldman Sachs estimates will be a breach of the IEA's 23-day critical inventory threshold — the point where rationing conversations start. The IEA's own director said in April that Europe had "maybe six weeks" of jet fuel left. Nineteen of the world's 20 largest airlines have already cut capacity. The UK appears most at risk of outright jet fuel rationing.

Refiners are responding the only way they can. TotalEnergies' CEO told investors the instruction to every European refinery is "max jet first." Valero bumped jet to 30% of its distillate output, up from a typical 26%. And the US is now shipping 150,000 barrels a day of jet fuel to Europe — six times the normal rate.

This is the tradeoff that almost nobody in the mainstream coverage is discussing. A refinery doesn't create barrels from nothing. When you push yields toward jet and middle distillates, something else gives. And that something is gasoline. US Gulf Coast refineries — the ones doing the heavy lifting right now — were optimized over the past decade to run light tight oil out of the Permian and Bakken. That crude is naturally richer in naphtha (gasoline's precursor) and leaner on the middle distillate cuts that become jet fuel. Asking these refineries to "max jet" means fighting the chemistry of the crude slate. Hydrocrackers help at the margin, but you're robbing Peter to pay Paul.

Refinery utilization sits at 91.6%. Solid, but not the 95-96% you'd want to see if you were trying to build gasoline stocks heading into summer. And even if refiners could push harder, the incremental barrels aren't going to domestic gasoline — they're going on tankers to keep European airports open.

So you've got two consumers pulling on the same barrel. The American driver filling up for a road trip. And the European airline trying to keep planes in the air. Both need product. Both need it now. The refining system is being stretched between the two, and the crude it's running wasn't really designed for what's being asked of it.

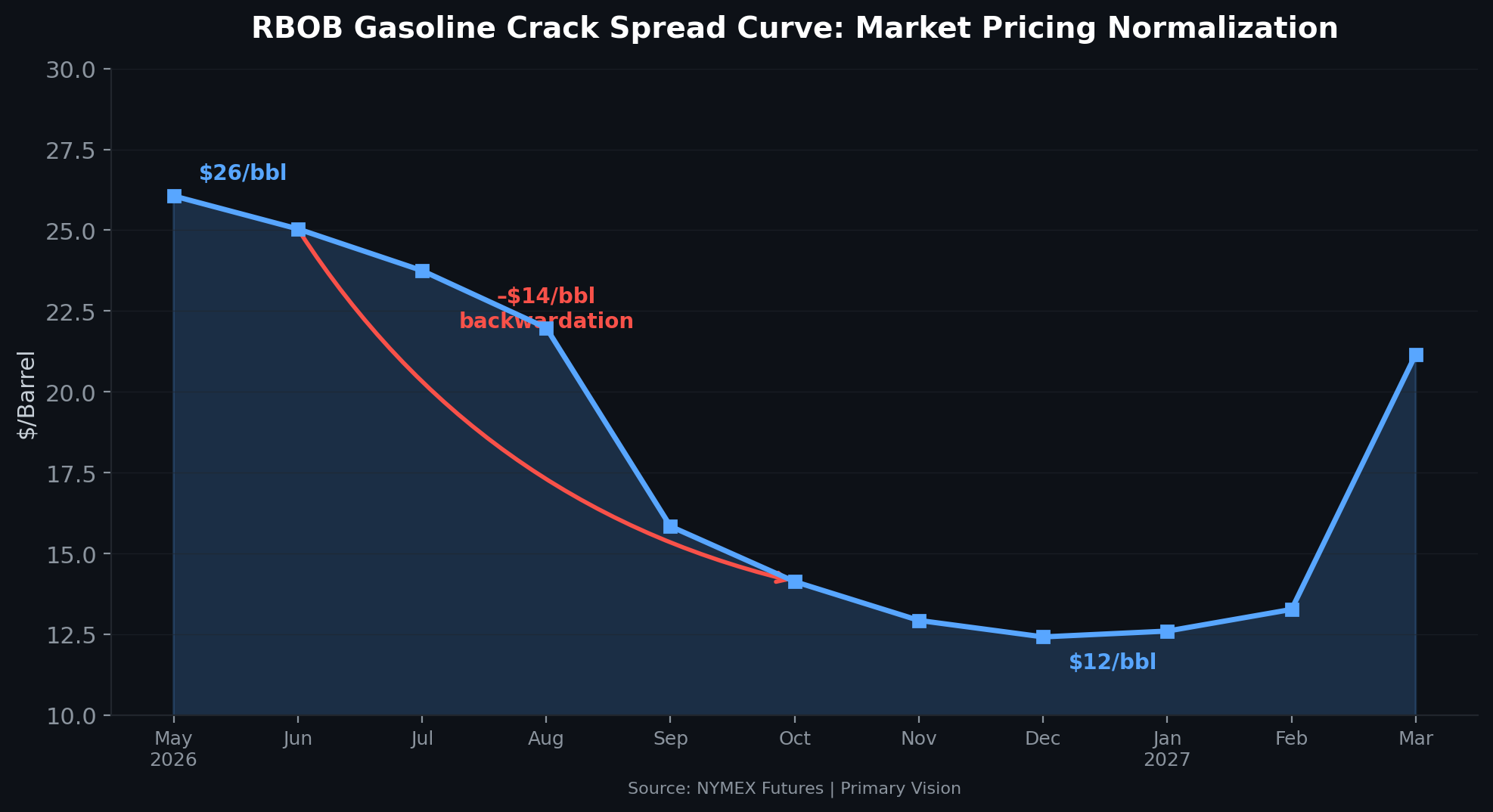

The RBOB crack spread curve tells you the market senses the near-term squeeze — May cracks around $26 a barrel — but the steep backwardation into Q4 (low teens) is pricing in an assumption that this normalizes. That's a big assumption. Even the optimists say a Hormuz ceasefire — and there are some early signals with a handful of tankers spotted transiting — would take two to three months before product flows actually normalize. ADNOC's CEO said this week that full recovery in Middle Eastern oil flows is unlikely before late 2027. That's not a typo.

Gasoline inventories at 214 million barrels heading into July don't rebuild in a week, or a month — especially not while refiners are still prioritizing kerosene exports across the Atlantic. A ceasefire headline can knock $10 off Brent in a session. But it doesn't put gasoline in tanks in Houston, and it doesn't put jet fuel in wing tanks at Heathrow. The product market operates on a completely different clock than the headline market.

That's the disconnect we'd be watching. Brent is trading around $105. The crude market has pulled back from the March panic. But the product market hasn't eased the same way — and heading into the highest-demand quarter of the year, with inventories already thin and refinery yields pointed in the wrong direction for domestic gasoline, the risk is skewed toward more tightness, not less.

Two consumers, one barrel. Something has to give.

Tags: