Articles

- BLOG / Articles / View

- Articles

Halliburton's Perspective in Q1 2026: KEY Takeaways

By Avik on May 4, 2026 in Articles

Industry Outlook

We have already discussed Halliburton's (HAL) Q1 2026 financial performance in our recent article. During the Q1 earnings call, management held the view that Middle East disruptions are likely to drive a sustained shift toward energy security and supply diversification. Several countries are expected to increase investment in domestic oil and gas development. Rebuilding global inventories will take years, with large cumulative deficits adding to structural demand. This supports a tighter market and a more constructive backdrop for commodities and oilfield services activity.

North America and Frac Outlook

In North America, frac calendar white space has largely disappeared, reducing concerns about activity slipping in 1H 2026. An increase in spot work inquiries suggests early signs of incremental demand and tightening capacity. The North America outlook is turning constructive, supported by stronger commodity prices and tightening premium equipment. The strategy remains focused on improving returns and pricing rather than adding capacity. Differentiated technologies like ZEUS IQ and e-fleets are expected to drive efficiency gains and enhance recovery for customers.

Middle East & Offshore Outlook

Middle East activity has been disrupted, particularly in offshore markets and key land regions such as Iraq and Kuwait. Halliburton continues to support customers while preparing for activity to resume as conditions stabilize. Supply chain disruptions have increased logistics and material costs, though management views these as manageable. The conflict impacted Q1 earnings by roughly $0.02 to $0.03 per share.

Outside the Middle East, offshore demand remains strong, driven by technology and execution capabilities. Overall, international momentum remains intact despite near-term uncertainty in the region.

Other International Activity & YPF Contract

International operations outside the Middle East delivered better-than-expected results and are expected to grow mid- to high single digits year-over-year. Latin America, particularly Argentina, is a key growth driver. Halliburton is leveraging its technology and integrated model as a competitive advantage across multiple regions.

The YPF contract in Argentina marks a major milestone, expanding its presence in unconventional completions. Deployment of ZEUS electric fleets and digital technologies is expected to support further global expansion.

Segment Forecast

Middle East recovery timing remains uncertain, with higher logistics and supply chain costs. It can impact HAL’s Q2 earnings by $0.07 to $0.09 per share. The Completion and Production segment is expected to see 4%–6% sequential revenue growth with modest margin expansion. In contrast, Drilling and Evaluation revenue is expected to be flat to slightly down, with margins declining due to seasonal software sales roll-off.

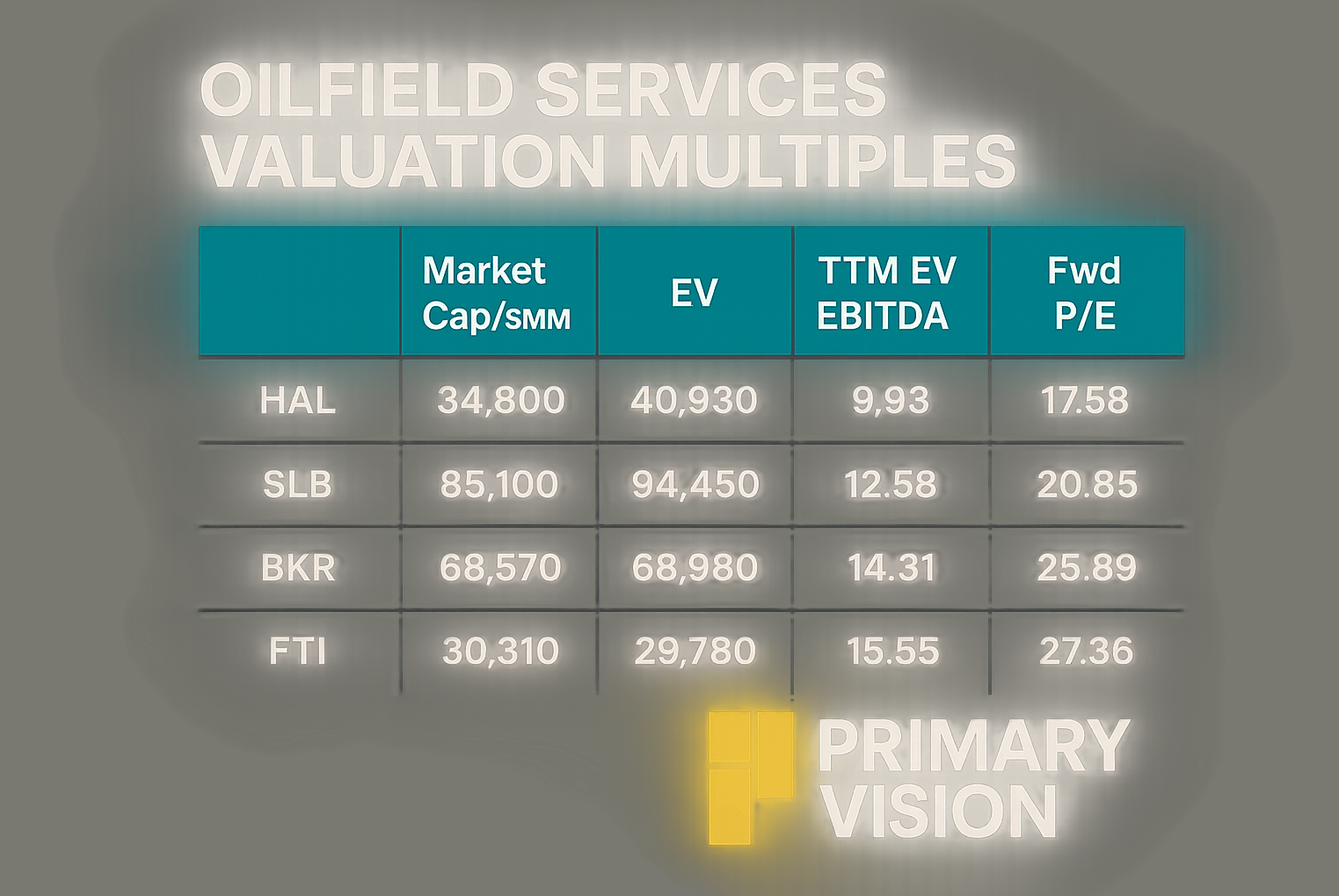

Relative Valuation

Halliburton is currently trading at an EV/EBITDA multiple of 9.3x. Based on sell-side analysts' EBITDA estimates, the forward EV/EBITDA multiple is higher. The current multiple is lower than its five-year average EV/EBITDA multiple of 9.8x.

HAL's forward EV/EBITDA multiple expansion versus the adjusted current EV/EBITDA contrasts a decline in the multiple for its peers because the company's EBITDA is expected to decline versus a rise in EBITDA for its peers in the next four quarters. This typically results in a much lower EV/EBITDA multiple than peers. The stock's EV/EBITDA multiple is lower than its peers' (SLB, BKR, and FTI) average of 14.2x. So, the stock is reasonably valued compared to its peers.

Final Commentary

It appears the global outlook is improving, with Middle East disruptions reinforcing energy security and supporting a tighter supply-demand balance. North America is turning constructive as frac calendar gaps close and early signs of capacity tightening emerge.

However, Middle East disruptions continue to weigh on near-term activity and costs, creating earnings headwinds. International markets outside the region remain strong, led by Latin America and supported by technology-driven demand. Overall, Halliburton’s technology, international exposure, and disciplined North America strategy position it well for gradual growth despite near-term volatility. The stock is reasonably valued compared to its peers. Form

Tags:

Permission denied

Upgrade to Pro Today and get…

• This article — plus dozens more each month, all within our full Research Module

• Frac Hits — our National-Level Frac Spread Count and Frac Job Count, updated weekly

• Frac Operator Monitor — detailed FSC & FJC by operator

• And so much more, designed to help you track, forecast, and outperform